TAPAS.network | 8 May 2024 | Commentary | Beate Kubitz & James Gleave

Where is MaaS going? Its complicated…

Mobility as a Service has been an idea that’s time has supposedly come for a decade or more. However it’s not hit the mainstream, and one of the companies that has led the way in developing the concept has just gone bust. Is it being stopped from taking off? Will it ever deliver the benefits for easy- to- use multi modal travel that its advocates believe are possible? The authors of a new book on MaaS, and , outline the current state of play, and the prospects.

BARELY HAD THE INK DRIED on our book - Mobility-as-a-Service: Its development, deployment, and future - when the news dropped. MaaS Global, the Finnish company behind the Whim app and one of the most long-standing and well-known companies advocating the MaaS concept, was going bankrupt. Since that news broke, MaaS Global was acquired by umob, from the Netherlands, but the collapse raised the inevitable questions. MaaS has been around for a long time, but where is it going now ? And what does the future hold?

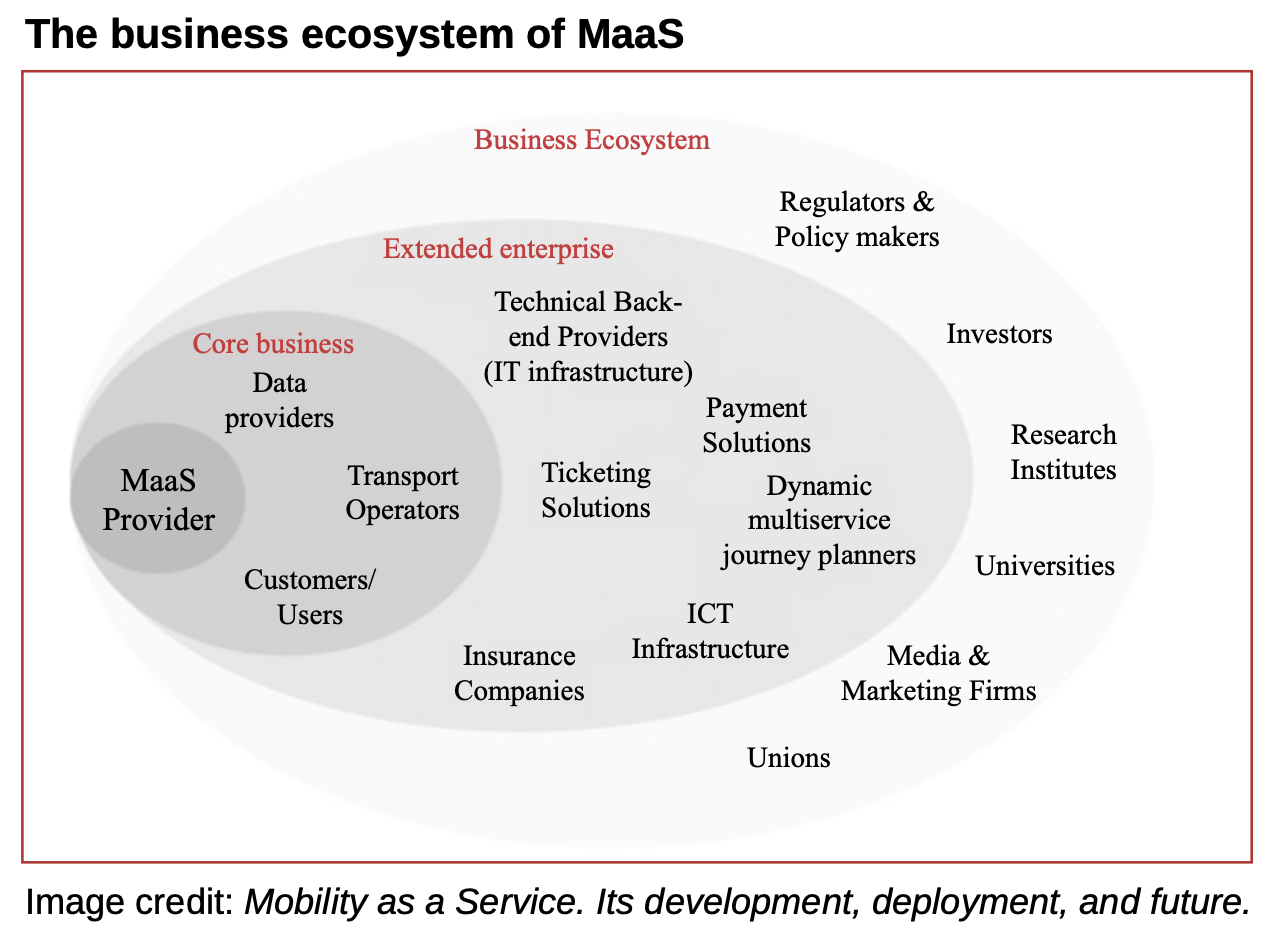

MaaS emerged as a concept from a variety of backgrounds, including the spread of integrated ticketing and online journey planners. Its definition originated (arguably) in a single university paper from Finland, but now encompasses a variety of digitalised transport services that have applied the name. Services that identify as MaaS have sprung from many origins – cities desiring next-level transport that enables them to function better, transport operators (both public and private) seeking new customers or market share, technology innovators seeking markets for their innovations, and academics validating their research and modelling. In its broadest definition, MaaS has originated in both public institutions and from entrepreneurs and private capital.

The result is a complexity and diversity of offers and operations under the MaaS flag, either having a wider appeal or serving a local need. For every global offer like Uber there is a Go-Hi (the MaaS platform launched in 2021 by the Highlands and Islands Transport Partnership HITRANS).

Breeze, which claims to be the UK’s first multi-city MaaS app covering Southampton, Portsmouth, and the Isle of Wight, introduced in 2022 in the Solent Future Transport Zone can be found in the app store alongside CityMapper and Google Maps . Each takes a slightly different definition of MaaS. Within this complexity, there are nonetheless some key lessons that have been learned that may help to shape what MaaS will ultimately become.

The first lesson is the role of the public sector and governance in developing MaaS. In some places, part of the role of the public sector has been to incentivise the private sector to lead in the development of MaaS through enabling works and incentives. The most notable example being the Finnish Transport Code, which has opened up data from many transport operators to enable the creation of new mobility services. In others, the development of MaaS solutions have been directly underpinned by public funding, such as the Department of Transport Future Transport Zones across England, as well as in the work of MaaS Scotland. In more still, MaaS solutions have sought to closely integrate with publicly-run public transport services, such as in Vienna and the Netherlands. All these MaaS models have had varying results in terms of commercial sustainability, and in increasing the number of passengers using the services they embrace.

This raises a further question about the role of the public sector in transport provision. While MaaS provides a service to the end user, it often does not solve more fundamental issues facing the quality and usability of transport services. Transport networks operate in the context of constrained resources (infrastructure, vehicles, and funding) with competing demands placed upon them by a population facing their own constraints and preferences. After all, a MaaS solution cannot, on its own, solve issues like traffic congestion, a silo mentality within operators, or competition laws making integrated ticketing difficult to achieve.

The second lesson, which has been learnt a number of times, is the complexity of the market MaaS must operate in. This reflects, in turn, the complexity of transport networks and geographies and cultures of particular places. The fact that, for example, providing transport services in rural areas is a fundamentally different challenge of that of serving urban areas is an obvious one. There has been a notable convergence within the private sector towards focussing on transport innovation in places where technological solutions can be applied at scale to serve a large number of trips relatively cheaply. This is notable within cities where the barriers to offering a wide variety of transport services (or a single or complimentary services at scale) on an integrated platform are relatively low.

This does not mean that MaaS service offerings outside of such areas are unfeasible, however, but that they require a more complex operational model than simply a single app provider integrating a variety of services. For example, there has been an extensive programme in Japan of developing MaaS solutions in primarily rural prefectures with close links to local bus services, demand responsive transport services provided by local government, and rail services provided by private companies.

The third lesson relates to understanding what objectives MaaS, and transport more generally, seeks to achieve. Within the UK, the approach outside of the Future Transport Zones and some pilots in Scotland, has been on the private sector developing solutions with the ethos that ‘the market decides.’ Often with MaaS solutions not seeking to achieve wider objectives outside of commercial success. Despite this, here has been some effort on behalf of local transport authorities, such as the West Midlands, to provide a strategic steer for MaaS-type solutions in their area, through practical measures such as simplifying ticketing and procuring bike share systems.

Beyond the UK , the approach has differed. In France, for example, the French Government introduced the loi d’orientation des mobilités, or French Mobility Orientation Law. Specifically for MaaS is the empowering of the Organising Authorities for Mobilities (AOMs) to include new mobility services under their jurisdiction. This includes car sharing, car pooling, and self-driving vehicles. The AOMs also are required to speed up the opening of all data sources for services under their jurisdiction. They are charged with coordinating the availability of data , and the transport regulatory authority (ART) with monitoring and settling disputes. But critically, this needs to be done in the context of achieving the goals of the new law, which include reducing the use of private cars, accelerating the growth of new transport modes, achieving the ecological transition, and scheduling investments in transport infrastructure.

Combining these factors and contexts paints a complex environment of MaaS, and for policy makers and transport professionals to navigate. That is mainly because it is a complicated and evolving environment, often full of new ideas, buzzwords, and a lot of confusion over the definition of MaaS – something which is still being debated. One firm conclusion that can be reached is that the technology to enable the delivery of MaaS is known and is widely available in many areas. Technological concepts like APIs and integrated platforms that were a novelty 10 years ago are now well established with which the majority of public and private sector organisations are familiar.

We can also conclude positively that combined digitalised transport service offers face relatively few barriers when it comes to consumer adoption, so long as solutions are provided that fit their needs. The likes of increased use of contactless payments on public transport, mobile phone ticketing, and even that the likes of Uber are finally turning a profit (after diversifying from simply providing digitised private hire) indicate a promising, if uneven , future for digital transport services.

We set out why we think with confidence that MaaS-style services will be part of the future of transport for years to come, because the concept has moved from an interesting idea into a tested and established service, even if it has not lived up to the ‘everything in one place’ vision quite yet. Transport systems and the trips that are undertaken on them are inherently complex, and consequently, the types of services that will be provided will reflect this complexity.

It is important for transport professionals to realise that MaaS is not a one-size-fits-all idea, or a single, integrated solution that will change the world all on its own. It is, however, an extremely useful tool for the digital age in which we live, and one that will change and adapt as the world around it changes. The question that we need to ask ourselves is ‘how do we use this tool to make transport, and the world, a better place?’the digital age in which we live, and one that will change and adapt as the world around it changes. The question that we need to ask ourselves is how do we use this tool to make transport, and the world, a better place.

James Gleave and Beate Kubitz have authored the new book entitled Mobility as a Service: Its development, deployment, and future. It is available from the Institution of Engineering and Technology

Beate Kubitz is a specialist in future mobility and the role it plays in carbon reduction. Her consultancy provides research, innovation and policy development at local and national level. As well as the new book on MaaS she has just co-authored, she also edited the Annual Survey of Mobility as a Service 2017-2020 published by Landor Links and is a regular contributor to transport journals.

James Gleave is a transport consultant and the founder and director of Mobility Lab, UK. He has assisted in the delivery of many transport and infrastructure strategies and policies and supported the delivery of various new technology, autonomous vehicles, smart infrastructure, and mobility-as-a service projects. He is also a board member of the Transport Planning Society.

This article was first published in LTT magazine, LTT891, 8 May 2024.

You are currently viewing this page as TAPAS Taster user.

To read and make comments on this article you need to register for free as TAPAS Select user and log in.

Log in