TAPAS.network | 3 December 2025 | Commentary | Pete Dyson

Has Government begun a new road use charging era with 3p-per-mile from EVs?

It was confirmed in the Budget that, from 2028, electric cars are to begin paying to use the highway system with a new 3p per mile charge, called eVED. explores the context of the decision, analyses the longterm financial, behavioural change and transport policy implications of this new type of motoring tax ,and speculates on how it may evolve in the coming years.

ELECTRIC VEHICLES (EVs) are seen by the Government as making a major contribution achieving its decarbonisation ambitions , but though increasingly popular , they have not as yet being paying anything equivalent to the fuel duty imposed on fossil-fuelled powered vehicles as they use the roads . This has in turn left a growing economic problem for the Treasury, in loss of revenue, and a sustainability gap for transport policy. “If we do nothing, then by 2030 around one in five car drivers are expected to pay no fuel duty at all… given all cars cause congestion and wear and tear on the roads, this is not a fair outcome” writes Dan Tomlinson MP, Exchequer Secretary to the Treasury, prioritising these issues above other negative externalities from car dependent transport systems.

While EVs represent the future, and are cleaner, the challenge remains to nurture their uptake while pursing wider economic, social and environmental objectives, and maintaining a crucial government income stream. Everyday, UK cars collectively drive just under one billion miles, equivalent to 6 times to the sun and back, so small changes to taxation add up to big differences (Dyson & Sutherland, 2021, pg 56).

The UK is the world’s first major economy to introduce a new pay-as-you- go mileage charge , not only addressing an fiscal issue from electrification, but opening up a new dimension for road user charging. We may , nonetheless, look back on this moment as a very significant point in the development of transport policy, if it first wins general public approval as an acceptable approach to user charging.

In the UK, electric cars now form about 25% of new sales and 5% of the total fleet. In principle, an EV tax could be reasonably popular, national polling commissioned by Stonehaven (October 2025) finding that “71% of the public believe EV owners should pay at least some tax, with only 14% saying they should pay none at all.” Likewise, in 2022, Campaign for Better Transport’s Pay As You Drive found general support for a flat rate tax. I expect Treasury officials and advisors read both, given the lack of government commissioned research on the topic (‘too toxic’ being the typical refrain). In my view the new charging policy is positive and pragmatic, effectively ‘splitting the difference’ between no tax and fossil-fuelled cars, and is a welcome coming-of-age for electrification. Contrary to accusation of being ‘confusing’, continuing the plug-in grant fund seems entirely consistent with making EVs a bit easier to buy, and then more equal to run.

Many transport professionals have called for much more radical dynamic ‘road pricing’, but this policy has been politically unpopular, and remains technologically untested. The 3p per mile charge is different and follows the 2017 paper Miles Better by Gergely Raccuja written for the Wolfson Economics Prize. Both his proposal and this policy follow principles of simplicity, fairness and transparency.

Here I analyse how the roll out might be framed, in the light of consultation now under way on its implementation, how it might affect different groups and how small changes can offer further improvements. I’ll also look at where this may lead in the longer term.

This article addresses three main questions:

(a) Why now and why 3p exactly?

(b) What behavioural policy principles are at play?

(c) How might these influence EV adoption, car use in general, and what future adjustments and extensions might be announced?

(a) What is the plan and why now?

-

The policy applies a flat-rate 3p per mile charge for battery electric cars and 1.5p for plug in hybrid cars. From April 2028, approved garages will record current mileage from EV and PHEV odometers, then vehicle owners will estimate and pay for the mileage in the coming year when paying VED, any difference in actual mileage being reconciled each year. The HMT Consultation document provides details and invites questions on how to handle the myriad edge cases rather than major changes to eVED’s design. The public and industry can submit views until 18th March 2026.

-

The precedent. In 2024, two countries have already introduced EV distance-based taxes. New Zealand introduced charges of 5.3p/mile for EVs and 2.6p/mile for plug in hybrids, with temporary exemptions for vehicles >3500kg (vans) until July 2027 and permanent exemptions for vehicles <1000kg (microcars). Iceland introduced a 5.4p/mile for EVs and 1.9p/mile for PHEVs in 2024 to all passenger cars and vans. Both countries electricity costs are roughly half the UK and their costs of motoring are also different, so comparisons are tricky. This year, Hawaii introduced a charge of 1.6p per mile (US$8/1000 miles).

Not coincidentally, these are all island nations so vehicle movements are much easier to manage.

Three continental European countries are considering a charge - Austria, Switzerland and Netherlands – but there large cross border connections and vehicle registrations are surely a big hinderance (something Northern Ireland officials will have to contend with too). -

The fiscal context. In 2024-25, existing road vehicle fuel duty will raise £25billion (Office of Budget Responsibility). If the current fleet of 1.7million EVs were fossil fuel vehicles, the Treasury would receive approximately £1 billion fuel duty. Based on DfT EV adoption forecasts (Climate Change Committee, Fig 7.1.3), the shortfall in fuel duty receipts from EVs in 2028 without any new charge would have been £3.1 billion/year and £7 billion from 2023-2027.

-

The proposed charge is effectively splitting the difference; OBR estimate “this charge is roughly equivalent to half the rate of fuel duty paid by drivers of petrol and diesel vehicles”, the Treasury probably see a fair compromise at the revenue collection level. At 3p/mile, the figure also puts the average EVs roughly midway between the cost of running a petrol/diesel vehicle (13p/mile according to HMT). This would be fairness and ‘splitting the difference’ at the user level. Thirdly, adding a usage charge while maintaining a purchase grant reduces the difference between EVs (expensive to buy and cheap to run) and petrol/diesels (cheaper to buy and more expensive to run).

-

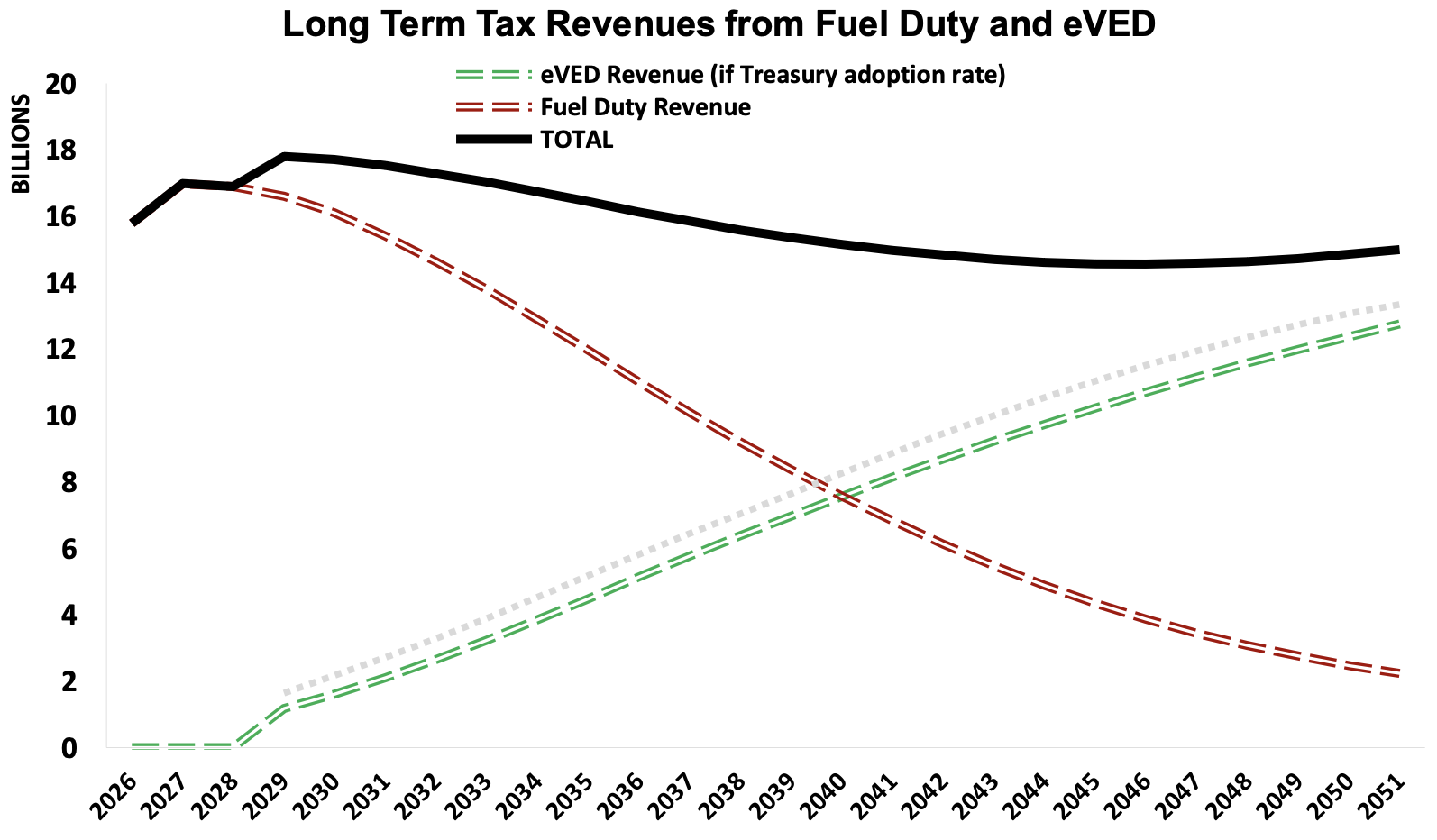

Long term cost of driving. If the 3p eVED charge rises with CPI inflation (forecast at +2% per year), then the cost will be 3.5p in 2037 and 4.5p in 2050. This remains much lower than the 6p mile in fuel duty currently paid by petrol and diesel vehicles,( and even lower if fuel duty also rises with CPI). With all forecasts also pointing to lower electricity prices, eVED puts the long-term trajectory for cheaper costs of motoring, which probably is not welcome news to transport planners concerned by car dependency, but is promising the cheaper motoring for those that want (and can afford) a car. We don’t know the future pathway of the government’s electric duty rate of course, the figure could change before introduction in 2028 and over the coming decades it is plausible eVED will be frozen in some years and get step change increases in others, just like the history of existing fuel duties.

Because fuel duty receipts dwindle as EVs take over, that starting point of a 3p charge pegged to CPI is extremely important in setting the trajectory. An extra +0.5p in 2028 accumulates to £27billion across 2028-2050, representing +£2.1billion per year in 2050. In the current forecast, eVED overtakes Fuel Duty receipts in 2040, just about 5 years after the UK fleet is expected to be 50:50 EV and fossil fuel cars.

At a revenue level, the graph below shows the long term revenue from car usage taxes remaining roughly constant (not adjusted for inflation). Assuming a stable 35million UK car fleet and car mileage per year, fuel duty increasing by 5p in 2027, and both eVED and fuel duty increasing by CPI from 2028 onwards, and the Treasury’s EV adoption rates (OBR, Chart 3.7).

Interestingly, the Treasury have shunned the Department for Transport’s own ZEV mandate projection, plotting slower EV adoption rates, leading to expecting £500million less receipts in 2028 and £16 billion less between 2028-2050. One suspects they would rather be pleasantly surprised by ‘fast’ EV adoption than go cap in hand to raise rates. Or as they say, the house always wins.

Plug In Hybrid EVs pay both fuel duty and eVED at 1.5p/mile, while comprehensive PHEV adoption forecasts are not available (to me), if we assume PHEVs represent 5% of all cars until 2035 (CCC forecast, pg 150) and remain at 5% to 2050, it adds £0.6 – £1.1bn per year (not shown below). Therefore, revenue from motoring usage taxation are forecast to be roughly constant (in 2025 money) between 2025-2050.

(b) Policy Principles: psychology and behavioural factors

How the charge will be paid

The eVED charge will be paid annually via the DVLA based on a driver’s estimated mileage, with an annual verification process. Drivers will estimate their total annual mileage and pay the corresponding charge when they pay their annual Vehicle Excise Duty (VED). Payment can be made as a lump sum or in instalments. The estimated mileage will be checked and verified each year, typically during the vehicle’s annual MOT test. MOT centres will record the odometer reading and submit it to the DVLA. If a driver underestimates their mileage, they will have to make a balancing payment for the difference, which may be added to their next VED bill. If a driver overestimates their mileage, they will receive a credit for the next tax year. Since new cars do not require an MOT for the first three years, owners will need to have a ‘light-touch’ mileage check at an accredited garage around the first and second anniversaries of purchase, with the government covering the cost of the check.

The government has stated the system will not require the use of invasive location- tracking ‘black boxes’ in cars, choosing the odometer-based system to protect driver privacy. The charge will apply to all miles driven by UK-registered vehicles,- including , interestingly ( and presumably unavoidably) those driven on foreign roads. The HMT Consultation does not disclose how much UK car mileage is overseas, but says it is “proportionate to prioritise privacy and simplicity over a system of checks to deduct non-UK mileage”.

Simplicity and transparency

The 3p/mile policy appears to mirror the strengths of the current fuel duty charge; simple, unavoidable and transparent. It is easy to understand and transparent for government, households and businesses to budget for. While a truer ‘fuel duty replacement’ would be a tax on electricity consumed by the vehicle, this would create inequity among those already enjoying near zero cost off-peak electricity and be very hard to administer. A flat-rate per mile creates a ‘floor’ so ensuring all vehicle use makes at least some tax contribution, irrespective of how it is fuelled, and therefore reflecting the in- use costs on the road network and its upkeep , congestion, air pollution and public safety.

Fairness and the ‘power of free’?

Within behavioural economics there is significant research on the ‘power of free’, also known as the zero price effect. Studies find it induces disproportionate demand and consumption (HBR, 2025)(Shampanier et al, 2007). While the Treasury estimates home charging at 27p/kWh, smart charging overnight when rates are cheap and the free rates from certain destination chargers (particularly workplaces) enable many EV drivers to enjoy exceptionally low rates of 0p, 1p and 2p per mile. If current EV drivers oppose this policy, it might be partly explained by research finding customers who enjoy free products often internalise this zero price as the reference point, making it hard for sectors to budge them to pay even a small amount (Pawels and Wiess, 2008). This phenomena is observed with car parking and the UK plastic carrier bag charge (House of Commons Library, 2024). I expect wider research on the price-elasticity of driving to surface too because the cost per mile looms large in people’s minds. While research finds people systematically underestimate the cost of driving overall (Andor et al, 2021), we are good at sensing regular costs but we often miss the costs of depreciation, servicing, tax and insurance (Gossling et al, 2022). By design, a cost per mile charge is among the least ‘stealthy’ ways to tax motoring.

Social norms: an institutional signal towards EVs

To many, a 3p charge may sound like a ‘push’ or ‘stick’ measure against EVs, but more optimistically, the policy may act as an institutional signal that EVs have reached a critical level of popularity and now require taxation to cover costs and further investment. The policy signals that they are now ‘the norm’, and research finds EV adopters are sensitive to social norms and rates of change (Higueras-Castillo et al., 2023). Such effects are difficult to evaluate, but lawyers (Sunstein, 2016) and environmental psychologists (Syropoulos et al, 2024) agree that policies are important instruments in signalling and guiding social change.

Will it reduce sales of EVs and even fossil fuel cars too?

This is possible, with increasing annual costs of ~£250-500 per year the OBR themselves estimate there will be approximately 120,000 EVs fewer in 2031 than without the policy (it would have been 440,000, but they believe the continuation of purchase grants and other EV incentives will boost sales by 320,000). If that 120,000 vehicle estimate seems low, consider that running costs are only 5th on the list of EV advantages cited by prospective buyers (DfT Tech Tracker, 2025, pg 14), and EV sales increased year-on-year in 2022, despite electricity costs more than doubling. More counterintuitively, because the ZEV mandate requires manufacturers hit annual sales proportion targets, a pure economic prediction will forecast EV prices fall to retain sales and fossil fuel vehicle prices rise in order to fund these discounts and prod customers to picking an electric car instead.

Policy packages and sequencing

There has already been £1.4billion provided in a plug- in car grant (2011-22), a further £650million in 2025, and an additional £1.3billion to continue this to 2030. Some may see collecting this 3p/mile charge as contradicting these plug-in grants, but it can be viewed another way: as a means to continue and extend the support to reduce the purchase price of EVs. Given that the charge arrives in April 2028, it’s really a ‘buy now and pay later’ signal for those on the fence, and a way of lowering the barrier to entry to getting an EV -which will also cascade down to reducing second hand prices- and slightly increasing running costs. Given the principal objection to EV equity is the high cost to purchase, this package seems entirely coherent rather than conflicting.

It also makes buying an EV more ‘like’ buying an ICE vehicle

This is because they’re now closer in comparison between purchase and running costs. Importantly, very low EV running costs have been making public transport less appealing, as the relative advantage of the EV at nearly 0p/mile makes any ticket price seem expensive by comparison. Ideally, this per mile EV charge could fund more targeted policies for EV equity for populations of specific interest, like extending a social leasing scheme for care workers (Campaign For Better Transport, 2025). Promisingly, research finds ‘policy packages’ – where new taxes are coupled with grants – increase public acceptability of climate positive measures, as people find them fairer and less punitive overall (Fesenfeld, 2022). A ‘quid pro quo’ strategy.

(c) Wider implications and potential improvements?

Beyond the flat-rate charge, I expect commentary on potential improvements to focus on four areas: efficiency, public charging equity, the plug-in hybrid rate and exemptions for vans.

Adjusting the rate to account for EV efficiency

While EVs have a total lifecycle climate change impact approximately 60-80% lower than petrol/diesel alternatives (International Council on Clean Transportation), they still vary greatly in their efficiency based primarily on size, weight, battery pack and driving behaviour. The Treasury published UK fleet average is 3.59miles/kWh, with efficient EVs nudging above 5miles/kWh and bigger EVs at just 2miles/kWh, so the variation is approximately +/- 40% around the mean.

Currently with fossil fuel cars, both annual vehicle tax (VED) and fuel duty send clear signals to incentivise vehicle efficiency and therefore their closely correlated dimensions of size, weight, air pollution, road impact and safety (Miner et al, 2024). Crucially, these are precisely the negative externalities that taxes on motoring are trying to internalise (not just to raise revenue to pay for road investment as the Treasury Consultation foreword promotes). Given the outweighed impact of charging large EVs on grid infrastructure, inefficient EVs remain more carbon intensive and more of a drain overall.

EVs just pay a flat rate for VED (£195/year) not based on size and efficiency and introduced in April 2025. Therefore, if eVED does not apply a factor for the vehicle’s efficiency, then there will be no tax signal towards efficiency and therefore size, weight, pollution and safety.

A solution to this could be to include EV efficiency as a multiplier in the annual EV mileage charge (as used by New Zealand for EVs and Switzerland for HGVs). A simple method would apply the industry standard for EV fuel economy (published range / useable battery capacity) and benchmarking this against the fleet average for the previous year: ie

Annual EV charge = annual miles travelled x £0.03 x vehicle efficiency

Where vehicle efficiency = [published range (miles)/usable battery capacity (kWh)]/UK fleet average efficiency from previous year (3.59kWh in 2024)

Most EVs would pay the 3 pence per mile, the most efficient (e.g. Renault Twingo, Tesla Model 3, etc) would pay 2 pence and the least efficient (e.g. Mercedes-Benz G 580) would pay 4 pence per mile. The formula above would use readily available automotive industry figures for efficiency, it would naturally move and improve over time (thereby keeping pace with technological improvements), it would be predictable for the Treasury, would encourage more efficient, safer and smaller EVs to be rewarded, and would open the door for included petrol/diesel vehicles into a per mile charging scheme too.

If not by EV efficiency metrics, I expect some commentators to advocate for adjustment based on EV weight. This policy is explained in detail by the Molden-Leach Conjecture from Nick Molden FRSC and Felix Leach in their book Critical Mass (2024). They find that, more than any other figure, weight correlates neatly with road safety, efficiency and other negative impacts.

Public vs. private charging

There is a current significant inequality between the cost of charging by private (domestic) and publicly provided charging facilities. This could be addressed by raising the planned charge by 0.5p/mile, to fund reduction of VAT on public charging from 20% to 5%. Or, given the Treasury’s conservative EV forecast, if adoption is hits the more optimistic DfT ZEV mandate pathway then there’ll be £500 million each year available to fund further EV improvements.

In this regard the introduction of an EV charge is an opportunity to flip a negative ‘tax’ on its head and ask positively , “what can we give to EV drivers that they cannot buy themselves?”. A better and cheaper public chargepoint infrastructure is surely high on the list. Adding 0.5 pence to make the charge 3.5p/mile would raise approximately £50 per EV per year and generate £500million in 2028. This would be sufficient to equivalise public charging VAT of 20% to the domestic charging VAT of 5%, and leave money left over to provide targeted funds for EV low-income support, improving chargepoint accessibility and wider public transport integration.

This is important for equity. At present, the 3p/mile charge tips the balance for public charged EVs to costing more per mile than petrol/diesel (based on HMT rates of 14p/mile for public charging).

Public charging is a shared resource; all EV owners gain because a small contribution from everyone could improve the public charge network in which they all have a stake, while also reducing inequity between those with and without home charging. At present, I suspect the current design banks on national electricity prices to come down over the coming 2 years to 2028, and for the public charge network to lead to reduced prices. So it will be interesting if others’ analysis of equity of this policy incorporates estimate of energy data and future price sensitivity into their modelling.

PHEVS and EVs: getting the balance of incentives right

The policy proposes 1.5p/mile charge for Plug-in Electric Vehicles (PHEVs), a vehicle technology that splits opinion between a ‘best of both’ bridging technology and ‘worst of all worlds’ delaying electrification technology. The balance of incentives is crucial here; too generous and the ‘bridging technology’ is over-adopted, crowds out EVs and is misused, too harsh and the PHEV technology which already underperforms on fuel economy becomes materially unattractive to all.

For context, new estimates show much worse real-world fuel consumption than advertised and this has not been accounted for in the VED and ZEV mandate figures. In 2024, the EU Commission analysed 600,000 vehicles’ in-car data and found PHEVs were on average 3.5 times (4 l/100km or 100 g CO2/km) higher than the type-approval values. The gap is mostly caused by overly optimistic assumptions about how often people will charge and therefore the share of electric driving mode (the ‘utility factor’, UF). Transport & Environment find PHEVs contribute nearly the same carbon impact as conventional hybrids and combustion vehicles in the real world, despite official emissions being 75% lower.

Ideally, a policy would align incentives, so PHEV drivers pay less if they drive more (or a minimum amount) in electric mode, and be incentivised to accrue credits to upgrade to fully battery electric cars. The purest solution would be in-vehicle data on electricity and fuel consumption, perhaps suggesting a higher (for example, 2p/mile) PHEV charge with the option for owners to reduce the annual charge by reporting their real-world economy. People may debate the fairness of PHEV drivers who seldom use their vehicle in electric mode continuing to receive the same incentives (lower VED regime and Benefit-In-Kind (BIK) as those who charge regularly. Encouraging PHEVs to be more efficient might prove among the cheapest ways the UK can hit decarbonisation targets, given people have the electric technology at their fingertips.

Exemptions for certain EVs, especially vans

The policy has been announced as the ‘Electric Vehicle Excise Duty on Electric Cars’ or eVED, which implies the 3p/mile charge applies only to cars, not vans, trucks, two-wheelers and buses. While current regulation on very small calls (microcars) is fluid, it is likely that UK manufacturers of <1000kg cars request being exempted to give this emerging category of more urban friendly vehicles a much needed boost (they otherwise have high purchase costs due to low production volumes).

Exempting vans will be important, because this segment is in need of urgent help to encourage electric power adoption (Van Fleet World, 2025). Unlike large SUV passenger vehicles, vans provide many essential business services and undergo high annual mileage, often in urban areas where electrification is most beneficial. Exemptions for vehicles over 3500kg until 2030 would follow New Zealand’s policy to delay EV charges for nascent segments. I am unconvinced by worries that fully exempting vans from 3p/mile could create perverse incentives, akin to what the USA experienced with light trucks when they enjoyed preferential rates following the 1973 oil crisis, leading millions to flock to this larger vehicle type and then stick with it. Personally, given just how tough the electric-van proposition is in 2025-2030, I imagine a policy could provide exemptions without tipping the scales too far in the wrong direction. The size of the pro-van lobby is likely stronger than the size of the anti-van counterpart, especially when re-enforced by increasing ‘domestic’ rather than business van use, as is a growing reported trend.

Conclusions: re the First Step in Charging EVs

The new EV charge is more than a revenue fix

If framed and packaged well, this policy move is a signal that electric driving has gone mainstream. It shows EVs are a valuable part of the system, and that system needs to evolve.

The 3p/charge is not road pricing as we knew it

Arguably it is the opposite, because a flat rate is charged per mile regardless of vehicle efficiency, location or time of day. A big strength, however, is the relative ease with which it could be replaced by a more advanced system in years to come. In that sense, it is technologically agnostic to future needs.

A flat rate is a start, but not the finish line

The next step should reward efficiency and keep costs fair for those without home charging. A more detailed design that flexes with efficiency, has exemptions and is slightly higher to reduce the public charge VAT could offer more refinement at only a small cost to the policy’s compelling simplicity.

The pence per mile figure might matter less than the direction of travel

Done well, this policy can balance fairness, revenue and sustainability. Done poorly, it risks stalling momentum just as EVs take off. This isn’t about taxing EVs — it’s about funding cleaner transport that can also be smarter, simpler and fairer for everyone on the road.

Conclusions: What May Come in the Future

Technology and taxation have at least one thing in common, everything looks impossible until it happens, then suddenly it looks obvious. People said UK government wouldn’t touch motoring taxation with a barge pole, but now it’s here.

From PCs to mobile phones, contactless payments to digital banking, club cards to frequent flyer programmes, congestion charging to smart meters; they all seemed impossibly expensive and unconscionable threats to personal privacy. But now nearly every household has them and they seem indispensable ways the modern world makes life a bit slicker and more rewarding.

Here are 4 speculative predictions:

Fuel Duty

Fuel Duty does rise in 2027, because eVED now closes the door on the principal objection that EVs are a ‘rich persons’ get out. It opens the door to regular small rises in fuel duty, providing overall headline inflation is kept under control.

Devolved powers

Devolved powers for congestion charging and tolls (aka ‘cordoning’). My estimates show EVs being consistently cheaper per mile to run. Meanwhile, costs of traffic in towns and cities remain high. Rather than the pure GPS based dynamic road pricing, I predict the incoming tide of devolution gives regional powers to set congestion charges, clean air zones, parking reforms that go into local funds (not general taxation). This significant revenue raising power could plug huge holes on funding, while enabling some local authorities to continue being pro-motorist and others to be more low-traffic.

Choice

The future of dynamic road pricing is now pro-choice. People may be offered a black-box style time-distance-place alternative payment option, with a pricing tariff to suit different needs. Akin to mobile phone usage contracts, some circumstances may make dynamic road pricing more appealing than eVED. In exchange, local authorities would get valuable origin-destination data to aid with transport planning. If passed through insurance companies with anonymity guaranteed, this may circumvent privacy concerns.

Beyond the UK

Beyond the UK, this distance based eVED will look very interesting, especially to island nations (e.g. Australia, Japan, Cuba, Sri Lanka) which are all keen to electrify transport (even if just to reduce dependence on oil) and this eVED charge from New Zealand, Iceland and now the UK looks appealing. Continental Europe requires alignment and cooperation to avoid people registering EVs in non-eVED nations, but this the EU and EECs raison d’être.

FOOTNOTES

-

EVs do already contribute a small ‘fuel duty’ type tax through VAT on charging, 5% for home charging and 20% for public charging. But the average EV (by efficiency and mileage) only currently contributes £33/yr in VAT if exclusively home-charged, and £248 if exclusively publicly-charged (assuming HMT Advisory Rates for home 27p/kWh and public 51p/kWh charging).

-

A private purchase of an EV incurs VAT (20%) like any other vehicle, but given the approximately £5000-10,000 premium on an EV relative to its fossil fuel equivalent, every owner has already made a contribution of approximately £1000-£2000 in tax revenues (equivalent to roughly 2-4 years of fuel duty money). (Businesses and company cars get more favourable relief).

-

The proposed charge narrows the relative difference between an EVs relying solely on public charging compared to home charging from +89% to +64% more expensive (Based on HMT Advisory Rates 2025). Cutting VAT on public charging from 20% to 5% would save an average distance EV driver relying solely on public charging (51p/kWh) £37 per year.

References and Links

-

Dyson, P., & Sutherland, J. (2021). (Referencing page 56) https://londonpublishingpartnership.co.uk/transport-for-humans/

-

Raccuja, G. (2017). Miles Better. (Written for the Wolfson Economics Prize). https://www.bbc.com/news/business-40600082

-

Stonehaven. (2025). (National polling commissioned in October 2025). https://assets.nationbuilder.com/stonehaven/pages/2141/attachments/original/1762962590/251113_Uneven_Road_Ahead_-_2025_briefing_2.pdf?1762962590

-

Campaign for Better Transport. (2022). Pay As You Drive. https://bettertransport.org.uk/wp-content/uploads/legacy-files/research-files/22.09.pay-as-you-drive-report.pdf

-

UK Government, Treasury (2025) eVED Consultation. https://www.gov.uk/government/consultations/consultation-on-the-introduction-of-electric-vehicle-excise-duty-eved

-

Office of Budget Responsibility (OBR). https://obr.uk/docs/dlm_uploads/Fuel-duty-supplementary-release_receipts-by-vehicle-type.pdf

-

Climate Change Committee (CCC). (Referencing Fig 7.1.3 and a forecast on page 150). https://www.theccc.org.uk/publication/the-seventh-carbon-budget/

-

HBR. (2025). (Referencing the ‘power of free’). https://hbr.org/2025/06/the-risks-of-offering-free-goods-and-services

-

Shampanier et al. (2007). (Referencing the zero price effect). https://pubsonline.informs.org/doi/10.1287/mksc.1060.0254

-

Pawels and Wiess. (2008). (Referencing zero price as a reference point). https://doi.org/10.1509/JMKG.72.3.014

-

House of Commons Library. (2024). (Referencing car parking and plastic carrier bag charge) https://commonslibrary.parliament.uk/research-briefings/cbp-7241/

-

Andor et al. (2021). (Referencing systematic underestimation of driving costs). https://www.nature.com/articles/d41586-020-01118-w

-

Gößling et al. (2022). (Referencing missing costs of depreciation, servicing, tax and insurance). https://doi.org/10.1016/j.ecolecon.2021.107335

-

Higueras-Castillo et al. (2023). (Referencing EV adopters’ sensitivity to social norms). https://link.springer.com/article/10.1007/s10668-023-03865-y#auth-Elena-Higueras_Castillo-Aff1

-

Sunstein, C. R. (2016). (Referencing policies as instruments in signalling social change) https://doi.org/10.7551/mitpress/11974.001.0001

-

Syropoulos et al. (2024). (Referencing policies as instruments in guiding social change). https://royalsocietypublishing.org/doi/10.1098/rstb.2023.0038

-

DfT Tech Tracker. (2025). (Referencing page 14). https://assets.publishing.service.gov.uk/media/66f3dc255316e21be6c4bc37/dft-tchnology-tracker-wave-11.pdf

-

Campaign For Better Transport. (2025) How Clean Transport Improves Lives for Carers and Clients. https://bettertransport.org.uk/blog/how-clean-transport-improves-life-for-carers-and-clients/

-

Fesenfeld, L. (2022). (Referencing policy packages increasing public acceptability). https://doi.org/10.1017/bpp.2022.3

-

International Council on Clean Transportation (ICCT). (Referencing EV lifecycle climate change impact). https://theicct.org/publication/electric-cars-life-cycle-analysis-emissions-europe-jul25/

-

Miner et al. (2024). (Referencing VED and fuel duty incentivising efficiency). https://doi.org/10.1016/j.jtrangeo.2024.103817

-

Molden, N., & Leach, F. (2024). Critical Mass. https://www.alumni.ox.ac.uk/article/critical-mass

-

Van Fleet World. (2025). (Referencing the need for help to encourage electric van adoption). https://vanfleetworld.co.uk/fleet-expectations-for-electric-van-adoption-declining/

Pete Dyson is a doctoral researcher at the University of Bath’s Centre for Climate Change and Social Transformations (CAST), iAAPS automotive and mobility research group, and co-author of the book, ‘Transport For Humans’. He was formerly Principal Behavioural Scientist at the Department for Transport, and is currently the Bicycle Mayor of Bath.

This article was first published in LTT magazine, LTT927, 3 December 2025.

You are currently viewing this page as TAPAS Taster user.

To read and make comments on this article you need to register for free as TAPAS Select user and log in.

Log in