TAPAS.network | 18 June 2024 | Commentary | David Leeder

Spending wish list for transport set to meet harsh post-election financial realities

The Transport ‘in tray’ facing the likely new Chancellor Rachel Reeves after the Election, will be overshadowed by the realities of harsh economics, and the pressure on public finances says . He takes a hard look at the economic and budgetary context, and how it will impact local transport, bus and rail policy, and funding, and suggests ten approaches which might help provide new solutions.

WHOEVER WINS the UK General Election on 4th July will face one of the most daunting economic in-trays of any UK government since 1945- and the implications for transport are likely to be far-reaching and severe.

The opinion polls indicate that Keir Starmer may deliver a Labour landslide comparable to Tony Blair’s in 1997, but he will inherit a budgetary and fiscal situation much closer to those facing his two post-war Labour predecessors - Clement Attlee in 1945, and Harold Wilson in 1974.

There has certainly been a lively debate over both main parties’ tax and spending plans, but the media and political narrative is generally incomplete and misleading. Whereas Blair inherited a sound foundation after 18 years of painful and often unpopular Thatcher-era spending controls, and restructuring of the economy, the Conservative led 2010-2024 government’s legacy will be rather different. It has managed, like Edward Heath in 1970-74, to become unpopular without stabilising the public finances, and despite huge rises in overall public spending. Notwithstanding the narrative laid at the door of Chancellor George Osborne and his successors, there has been no net ‘austerity’, even while some spending areas have been squeezed. Aggregate public spending is in fact at 75 year highs, NHS budgets have grown, and the tax burden is at the highest level since the 1970s - when the Heath and Wilson governments ran income tax rates above 80% and Corporation Tax above 40%.

Governments have access to tax revenues, and can borrow money from banks, financial institutions, and individual savers to fund their spending. The UK government (but not the members of the Eurozone) can also ‘print’ money via ‘quantitative easing’ (QE). This debt is then judged against the size of the economy (usually GDP), so Debt / GDP is a critical measure in a similar way that household mortgages are tested on a ‘loan to value’ basis. Since 1997, the UK’s borrowings have almost tripled, driven by three key changes:

1. The planned growth in public spending instigated by the 1997-2010 Labour government, which enlarged the public sector rather more than is generally understood, and which has not been rolled back in any substantial way

2. The unplanned cost of the 2008-2012 bank bailouts, which were essential to maintain the functioning of the economy, but came at huge cost in terms of additional debt, which the Cameron government managed to somewhat moderate in the 2010-2015 period

3. The extra debt incurred for the Covid lockdowns and medical response - also unplanned – relatively under managed, and thus hugely expensive - the scale of which seems not to be widely understood (perhaps because it was an economically essential, and superficially popular policy).

In 1997, when the Blair Government took over, the UK government had one of the better (ie lower) Debt/GDP ratios in Europe. Now we are closer to France or Italy in the ‘bad boy’ cohort, and much higher than Germany or much of northern and central Europe.

The cost of economic support during the lockdowns was comparable to the running cash cost of waging World War II. Like the bank bailouts, this is ‘money spent’ which not only has to be repaid, but which incurs substantial, and rising, debt interest costs.

The 2008-2010 bank crisis, and then Covid, led to over a decade when interest rates were at near zero (and negative in some countries) – literally at 200 year lows. The exit effects from a Covid lockdowns, and the Russian aggression in Ukraine, have led to an inflation spike, and a consequent huge percentage rise in interest rates, but which remain low by postwar standards. At first glance this seems paradoxical, but is a mathematical effect of the quantitative easing necessary to resolve the banking crisis.

The ‘normalisation’ of interest rates means that any household, company, or local authority with variable rate debt faces a higher cash interest cost, but the UK government itself now has the same issue – on debt that is approaching 100% of GDP. This is a major problem, even though current interest levels are historically low.

This means that in 2023, the UK Government is spending around 9% of its total budget on debt interest – roughly twice as much as the entire transport budget.

As mentioned, taxes have been well in the spotlight of this election campaign- but the political debate has missed one key dimension. The UK discussion about taxes often suffers a lack of realism about ‘dynamic effects’ – something that anyone who has ever been involved in making bus or rail fare changes will be familiar with, through the concept of ‘elasticity’.

The issue is not just ‘how high can we push prices (or taxes) politically’ but ‘what is the dynamic response in behaviour of those paying higher levels’ , and what does this mean for tax yield and other consequential actions ?’. Raising taxes, or bus fares, is always the easy bit, but does not guarantee that there will be a ‘100% yield’. The dynamic effects from tax rises include people leaving the country (the famous Non Doms) or cutting back working hours and overtime (eg the NHS doctors caught in the ‘pensions cap’, now abolished by current chancellor Jeremy Hunt), or deferring house moves (to escape high Stamp Duty). All but the smallest companies have just been hit with a major hike in Corporation Tax ( which has risen from 19% to 25%) - not a ‘6%’ rise but actually 33% This is a direct cash hit to funds available for re-investment and the distribution of shareholder dividends which – to state the obvious – is the ultimate reason why anyone invests in company shares. The UK has thus moved from one of the lower corporate tax regimes in Europe, to ‘mid table’, further reducing competitiveness.

Meanwhile, many more ‘ordinary, hard-working’ families are being dragged into the 40% tax band by the ‘fiscal drag’ of failing to index allowances, so that this segment has increased from 6.5% of taxpayers in 1990/91 to 18% in 2023/24- causing both political pain and a squeeze on personal spending .

How much more will the public (and businesses) accept in additional taxes before incentives for work and economic growth are blunted?

The rise in health and social spending crowds out transport

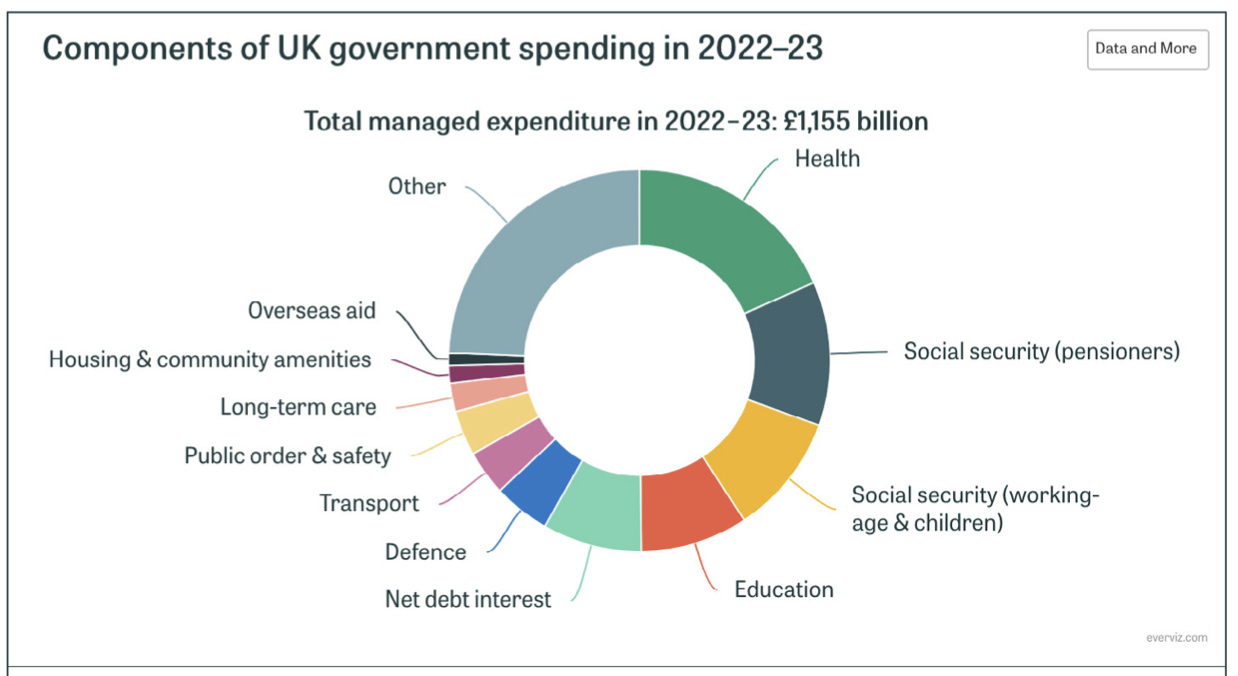

Transport spending is probably a priority amongst the readers of this article, but that’s not the usual view of Governments and citizens more generally. Indeed taken together, spending on pensions, health and social security are the priority areas – which now amount to around 40% of government spending. This is roughly ten times the entire transport budget (see chart below). This segment is heavily exposed to structural pressures – an ageing population, and the development of new, but expensive health treatments - and is both labour-intensive and heavily unionised. The internal pressure within the wider Labour movement to reward staff with above-inflation pay settlements will be immense.

The new government will face similar pressure from other spending departments including – in no particular order – the costs of meeting past claims for local government wage differentials, and demands for substantially increased miliary spending to challenge Russian and Iranian aggression.

A squeeze on transport looks inevitable, as even small increases in health, social or defence spending run the risk of ‘crowding out’ transport projects, large and small. The post-election spending rounds will be challenging for all departments, including Transport, which, beyond the sector itself , will not always seem a priority area to MPs or, more specifically to a new Chancellor like Rachel Reeves.

Despite the public commitments of Starmer and Reeves to financial discipline, it seems improbable that Labour MPs or their allies in local government or trades unions will be pushing for draconian cuts to salary or capital budgets, or dramatic restructuring of public sector wages, pensions or staffing. The pressure will instead be to increase spending to meet Labour’s social and environmental goals.

Labour has signalled a return to the (Gordon) Brownian notion of ‘we will borrow to invest’, but this is a somewhat artificial distinction, since the debt incurred will be secured by the UK taxpayer, and not against specific assets. Global debt investors are unlikely to make any such distinction between ’capital’ and ‘current’ spending – to them it is just ‘more debt’, and will look at the totality of UK borrowing. Any market alarm about the Debt/GDP ratio will manifest itself as either a buyers’ strike for bonds, and or increased interest rates (to get the new bonds away). This was the crisis that faced Liz Truss two years ago, and Labour in the 1970s.

Labour in government does, however , have some room for manoeuvre, although each option will bring political challenges:

1. It can raise national taxes, without breaking pre-election pledges, by the tried and tested approach of not indexing personal allowances. The top 1% of earners already contribute around 30% of the entire tax take, so there are limits to how much further they can be squeezed. The problem here is that more and more people are being sucked into higher rates of tax, including occupations such as train drivers and teachers who most people would not consider ‘rich’ and who form part of Labour’s traditional core vote. Raising tax yield – even by stealth – from the current, elevated levels will be neither easy, nor politically popular.

2. It can authorise more local taxes and charges, by allowing Council Tax to rise, and by expansion of local ‘charges’ on congestion, emissions (ULEZ etc), second homes etc to help pay for new local bus, rail and long-promised rapid transit schemes . The problem with such approaches is that they go against both ‘the cost of living crisis’ and the ‘levelling up’ agenda. They also impact the cost of doing business in Britain’s regions and metropolitan areas , which are already falling behind not just London and the South East, but even parts of central Europe. What may be (reluctantly) acceptable in London may not work around the country, where households are both, on average, poorer and more likely to use cars, so political and practical caution is likely needed here.

3. It can bring in new sources of revenue by new taxes and charges on economic ‘bads’ both to drive behaviour change (eg on smoking/vaping and sugary drinks) and meanwhile boost the Treasury coffers. Most of these would be insignificant in revenue terms, but a further look at ‘Pay As You Go’ road user charging seems inevitable, as fuel taxes from motoring dwindle with the shift to electric vehicles. This will be politically challenging, given heavy car use outside London, including by lower income workers.

4. It can broaden the tax base, by further taxes on saving, pensions and investment, by capping or restricting pensions, ISAs, Venture Capital Trusts and other tax efficient savings schemes. Labour think tanks have recently noticed that it is ‘the rich’ households who save the most (who knew ?), but big changes here will fall heavily on the mass affluent ‘swing voters’ that Labour would need to win again in 2028/29, and would also cut the supply of capital for Britain’s struggling stock market – especially for the smaller high tech and green energy businesses on which future growth depends.

5. It can direct private capital and savings. Labour could legislate to force pension funds to hold more UK government bonds (debt), and or it could force pension funds to co-invest in green energy and transport infrastructure that meet Government’s objectives. The cost here would fall on savers, who would be forced to accept lower-than-market returns, and therefore ultimately poorer retirements, but who might not notice the effects for decades (if ever). I suspect that this will be a major focus of Labour policy, given widespread ignorance about how pensions are funded.

6. It could offer tax incentives for private investment in transport, and energy transition schemes. This is a version of 4 above, but achieved by incentive, and not coercion. For example an extra ‘green transition’ ISA or additional pension saving could be offered that gave savers tax relief on investment in green energy and similar projects, including transport. This might be far more acceptable to the middle classes, but could be portrayed as helping ‘the rich’ (who of course tend to be the people who save and invest), and would also require Labour to accept a continuing role for private investment in energy, water, transport and other sectors with which the Party has traditionally been uncomfortable. In my view this could sugar the pill with the middle classes, and allow global capital pools to participate in some transport projects.

7. It could allow local authority-controlled transport authorities to borrow directly from the markets. This occurred under the Blair/Brown government, for example with TfL and Network Rail bonds, and has also been common in France. The limit here is that few investors now believe that this is not really UK Government debt. I was once told that French railway debt is – quote – “visible from the moon”. TfL debt is going in a similar direction. The problem for Rachael Reeves would therefore be to convince investors that the UK Government is not ultimately responsible, and that therefore such borrowing is not just “disguised” UK debt. This battle was lost long ago with Network Rail, and the government no longer even tries to pretend that NR is not owned by the state. It will be no different with the arrival of Great British Railways.

8. It could revive the Public Finance Initiative – probably under a new name. This approach would work well with 5 and 6, above. This would also require the Government to convince the markets that this debt is not ‘on balance sheet’. Private borrowing of this kind will always be more expensive than ‘pure’ state debt, let alone non-repayable capital grants to local government. But ‘perfection should not be the enemy of the good’, and some kind of ‘PFI’, but with incentives better aligned to project outputs, and a fairer allocation of risk, could offer advantages. For example:

Getting specific transport schemes off the ground quickly, that would otherwise be fighting for budgets with the NHS, social care and defence

Allowing the private sector to contribute ‘good ideas’ for transport in specification and execution to reduce costs or grow patronage, rather than simply using them as a source of borrowing.

This requires very careful project structuring, incentives that link to the end-goals for the public sector (eg climate, passenger growth and decongestion), and a willingness to loosen project design specifications. There certainly are lessons to be learned from PPP/PFI that are more subtle than “government grants are cheaper than private borrowing”.

This could be a challenge for Labour and Labour local authorities who seek ‘control’ as a goal in itself. Nevertheless, the prize is large. We saw in the late 80s and early 90s how pragmatic transport authorities could grab this opportunity – and the existence of the Manchester Metrolink (and the lack of such schemes in (say) Bristol and Leeds) reflects that city’s willingness to take the ‘best deal available’, rather than no deal.

9. It could take an axe to highly expensive transport infrastructure projects eating up substantial public spending with questionable Benefit Cost Ratios. Rishi Sunak began this with cancelling the Northern legs of HS2 , and there have already been calls from the ‘Green Left’ to stop multi-billion road schemes like the Lower Thames Crossing, the A303 Stonehenge Tunnel project and the A66 upgrade (as reported in LTT magazine, LTT893, 5 June 2024). The sheer size of some of the large road and rail projects, and the large percentage of the budget overruns, will force some kind of reconsideration.

10. It could authorise new kinds of hypothecated local taxes on residents, transport users and businesses and property developers to fund specific projects. For example, Land Value Uplift Capture like that employed to help support the development of the Elizabeth Line – which luminaries like Lord Hendy ( late of TfL and now Network Rail ) are saying did not extract as much from the private sector beneficiaries as they should have done ( also see LTT magazine, LTT893, 5 June 2024). The problem here is the stark difficulty of applying such ‘development taxes’ in regions which are already underperforming economically, and which must compete for developer funding not just within the UK, but at a European level. Transport specialists should be prepared for disappointment if local voters, when asked to pay for capital schemes directly through local taxes, rather than receiving ‘free’ HMT capital grants, decide that they don’t really want them.

Conclusions

I hope I have demonstrated that the public sector spending situation facing the incoming Government is very difficult , but there are plausible pathways for transport to navigate and mitigate this. The challenge for the sector will be to create financing structures that buffer it from the broader public spending challenges around health, social security and defence, and create new structures that allow longer-term sources of funding to meet societal goals for regional economic growth and environmental improvement, in which transport can play a key part.

The weakness of most of Britain’s regional economies outside London & the South East implies a reliance on transfer payments (ie new tramways in Yorkshire are likely to be funded from taxes raised from Londoners), and a caution in raising local taxes on city regions that are already struggling. The limitation is the ability of the broader south (a region bounded by Bristol – Oxford – Cambridge – Brighton – Bristol) to fund all this spending.

Tagging projects simply as ‘essential infrastructure investment ‘will not cut the mustard in this new landscape, where the need is to truly demonstrate real rates of return and value for money, and be ‘affordable ‘ and ‘fundable’ and not just tick traditional business case boxes. This means a new playbook for unlocking transport spending and resourcing that helps get things done differently to address the specific challenges within local transport, rail and bus provision, and offer prospective creative solutions to them.

David Leeder is co-founder of consultants TIL Transport Investment Ltd, and was previously a director of National Express Group, West Midlands Travel, FirstGroup and Greyhound Lines, USA.

This article was first published in LTT magazine, LTT894, 18 June 2024.

You are currently viewing this page as TAPAS Taster user.

To read and make comments on this article you need to register for free as TAPAS Select user and log in.

Log in