TAPAS.network | 13 November 2024 | Commentary | John Siraut

Rail use is growing – but is split ticketing inflating the estimated passenger numbers?

Rail passengers numbers seem to have been bouncing back further since the big falls due to the pandemic. But are the figures being announced by the Office of Rail and Road telling the true story, based as they are on ticket sales rather than monitored actual journeys. looks at the impact of the ‘split ticketing’ issue by which users save money by buying more than one ticket for a single journey

THE LATEST DATA from the Office of Rail and Road (ORR) records that passenger numbers on the rail network continue to grow after the severe hit they took during the pandemic. ORR reports that a total of 420 million journeys were made by rail passengers in Great Britain in the latest quarter (1 April to 30 June 2024). This is a 7% increase on the 392 million journeys in the same quarter in the previous year (April to June 2023). For comparison, the figures for the same quarter in 2019-2020 before the pandemic struck totalled 438 million.

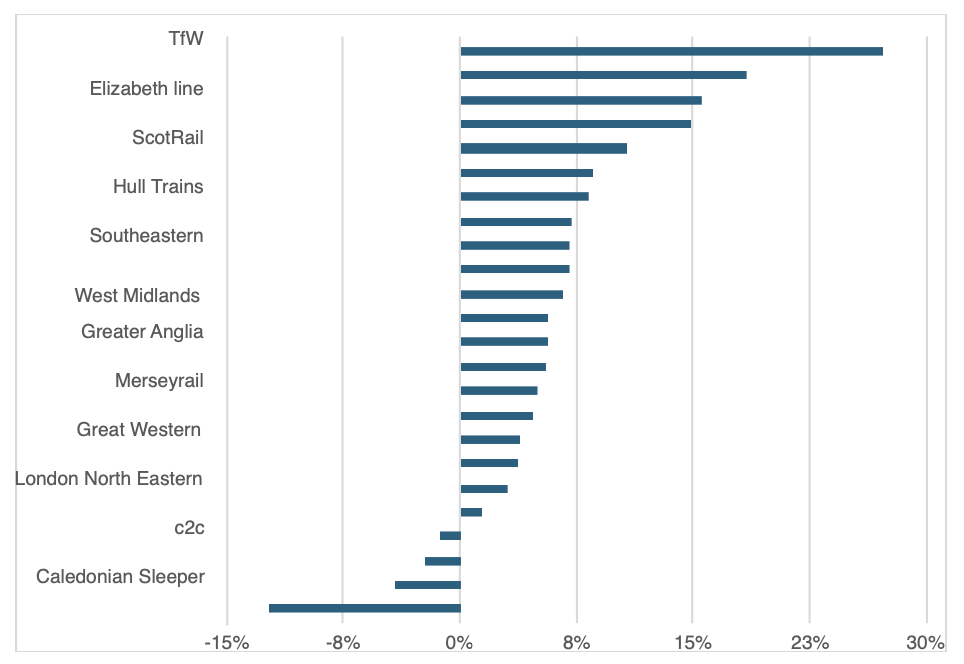

Figure 1 shows percentage growth in journeys by train operating company (TOC) in the 12 months to June 2024. Across the network the number of passenger trips grew by 7.1%. Transport for Wales and TransPennine saw very impressive growth while usage of the Elizabeth line continues to grow strongly. Open access operators Lumo and Hull Trains also posted above average growth as did ScotRail, partially because of its peak fare removal pilot.

Heathrow Express continues to lose passengers to the Elizabeth line, while Grand Central and London North Eastern saw their post pandemic boom start to unwind.

Figure 1: Percentage change in passenger numbers Q2 2023-Q2 2024 by train operating company

Source: Office of Rail & Road https://dataportal.orr.gov.uk/statistics/usage/passenger-rail-usage/

Department for Transport daily use data meanwhile shows that growth has continued between July to September 2024 with passenger numbers up 9% on average compared to a year ago – both on the whole network and the network excluding the Elizabeth line. Figure 2 shows the14-day moving average as a percentage of pre-pandemic levels. The upward trend is clearly visible.

Figure 2: Passenger numbers as a percentage of pre-pandemic levels including and excluding the Elizabeth line, 14-day moving average.

Source: Department for Transport https://www.gov.uk/government/statistics/transport-use-during-the-coronavirus-covid-19-pandemic

Various commentators have wondered whether the stated increase in passenger numbers recorded in the ORR statistics (which is based on tickets sold rather than journeys made) is partly because of the growth in split ticketing. Split ticketing, by which travellers purchase a combination of tickets to get between points A and B to minimise the total cost of their journey has been around for a long time, but its use was generally limited to those few who knew their way around Britain’s complex rail ticketing system. RailEasy’s launch of its TrainSplit website in 2014 introduced split ticketing to the wider public, highlighting its potential for considerable savings. Now it is widely used. Is the recent ‘increase in rail trips’ due to a genuine rise in demand, or is it because more people are now purchasing multiple tickets for a journey where previously they would have just bought one, thus recording it under the industry’s measuring system as multiple trips instead of one?

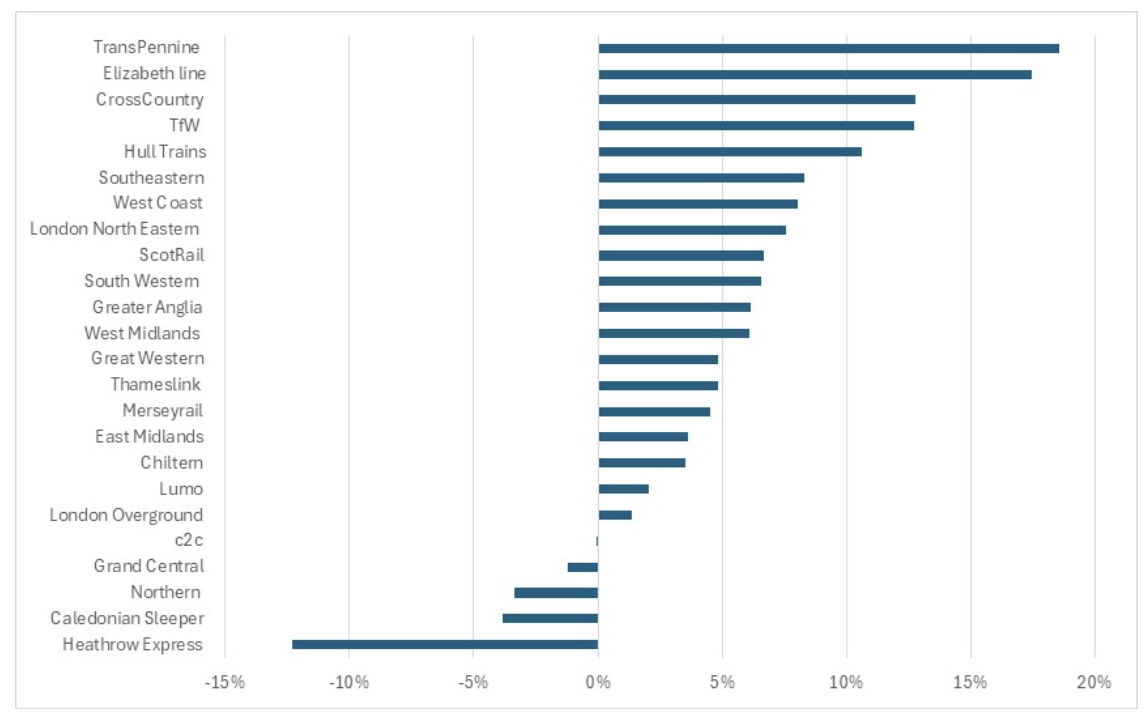

As well as reporting the number of rail journeys made by each operator, the ORR also publishes data on the number of passenger kilometres travelled. Figure 3 shows the percentage change by operator in the 12 months to June 2024. Overall passenger kilometres travelled increased by only 6.5%, which is 10% less than the 7% increase in the number of trips.

Figure 3: Percentage change in passenger kilometres Q2 2023-Q2 2024 by train operating company

Source: Office of Rail & Road https://dataportal.orr.gov.uk/statistics/usage/passenger-rail-usage/

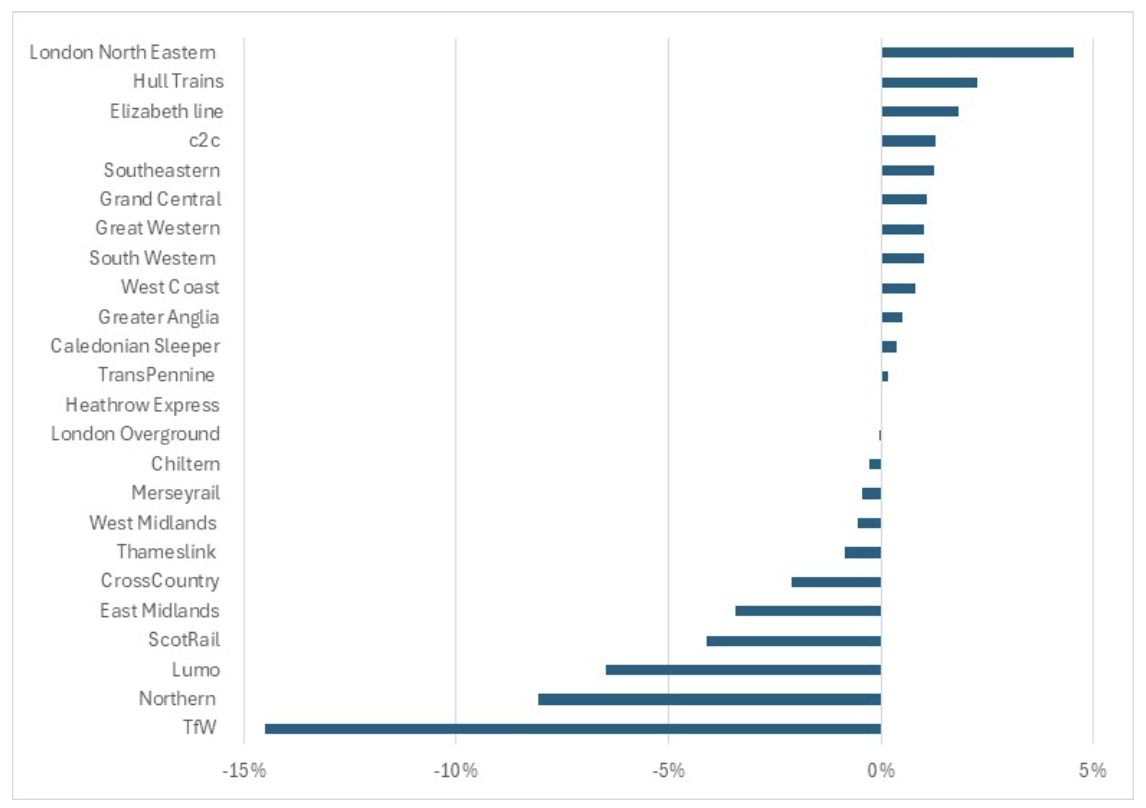

To make comparison easier, figure 4 shows the percentage point difference between the change in passenger journeys and passenger kilometres by TOC, using the ORR data. A positive number shows passenger kilometres increased more than passenger journeys, that is average journey length increased. A negative number shows the opposite, i.e. average journey length decreased. For the majority of operators, the difference between both measures is within the range of plus or minus two percentage points suggesting average journey lengths have remained broadly constant. Transport for Wales, Northern and Lumo have seen average journey lengths reduce significantly, while London North Eastern has seen an increase.

Figure 4: Percentage point difference between change in passenger journeys and passenger kilometres Q2 2023-Q2 2024

Source: Office of Rail & Road https://dataportal.orr.gov.uk/statistics/usage/passenger-rail-usage/

Given this analysis covers just one year, it does not allow any firm conclusions about the effects of split ticketing. Data on the extent of split ticketing is not publicly available. However, an analysis of one million recent RailEasy ticket sales reveals that two-thirds of journeys costing over £50 use split tickets, while less than a fifth of journeys under £20 do. While RailEasy ticket sales are likely to be more skewed towards split ticketing than the overall market, it illustrates that split ticketing, as might be expected, is likely to be most used on higher cost and longer distance journeys.

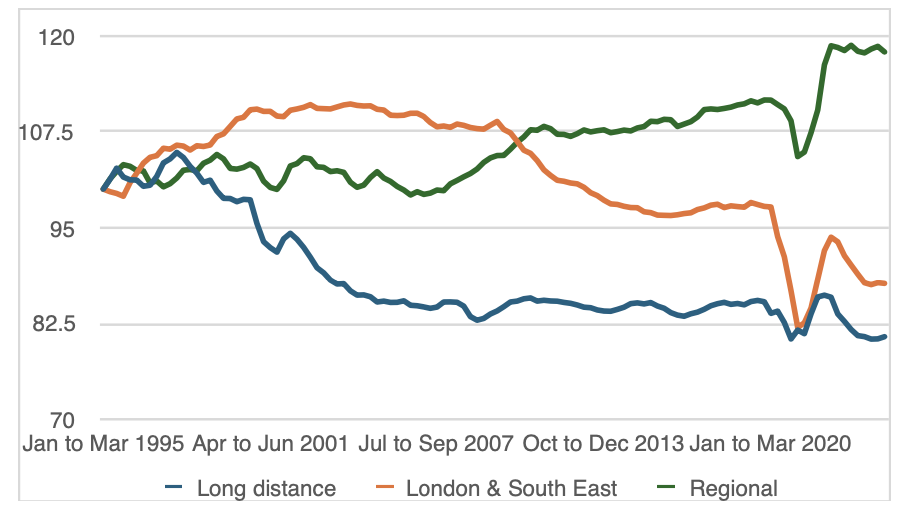

From the ORR data we can further derive average journey length by the three sectors into which the rail market is historically split. That is, long-distance; regional; and London and the South East. We can then observe how this has changed over time, (figure 5). This shows a four-quarter moving average, to remove seasonality. As can be seen, the three sectors have moved in different ways. The regional sector has seen a steady increase in average journey lengths, and a more marked increase after the pandemic. This latter increase is in part driven by a reduction in short distance commuting trips into major cities such as Manchester and Glasgow, as people moved to hybrid working involving both working from home and attending their workplace. In the London and the South East sector, average journey lengths had increased until around 2010, then steadily declined until the pandemic. After that, unlike the regional sector, average distances declined further. This is likely to reflect the fact that it is longer distance commuters that are increasingly likely to work from home, and also the impact of the Elizabeth line with very high volumes of short journeys. The long-distance sector meanwhile saw a steady decline in journey lengths until around 2008. However, from then until the pandemic, average journey lengths remained fairly stable and are now slightly below pre-pandemic levels, although 20% lower than in 1995. Trainline, the largest on-line retailer introduced split ticketing in 2020, which could be reflected in the further reduction in average distances for long-distance journeys. However, this may also be due to changing travel patterns post pandemic. From this data set it is difficult to determine if split ticketing has had a material impact on the increase in the number of recorded journeys.

Figure 5: Index of average journey length by sector, four quarter moving average Apr 1994- Mar 1995 =100

Source: Office of Rail & Road https://dataportal.orr.gov.uk/statistics/usage/passenger-rail-usage/

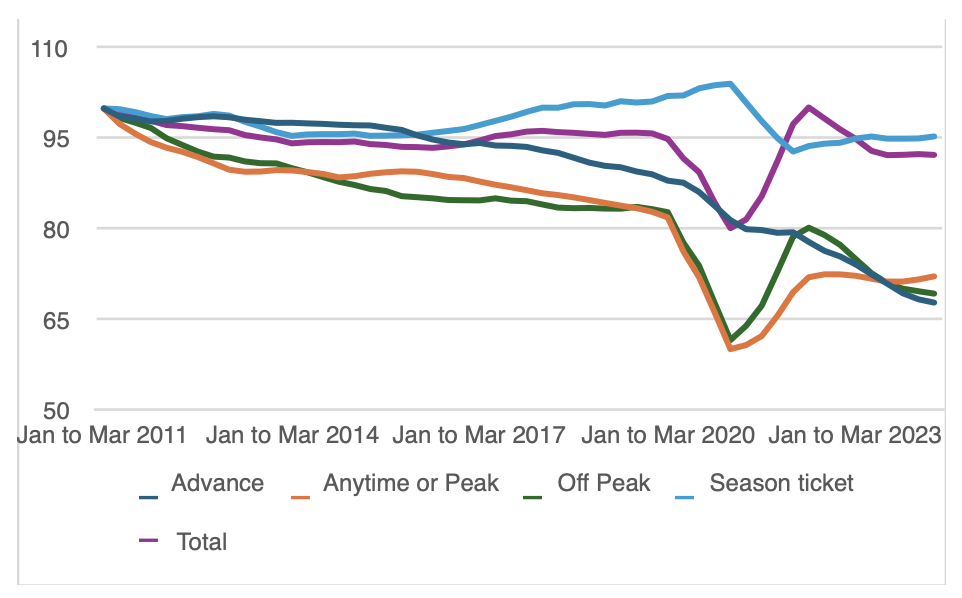

The next step on this analysis, therefore, is to look at how average journey lengths have changed by ticket type. This shows a rather different pattern, (figure 6.) Data here only goes back to 2011 and again is presented as an index using a four-quarter moving average. Average distances travelled have fallen steadily across all ticket types, except for season tickets, which grew from 2016 until the pandemic. Advance tickets saw a gradual decline in journey length up until the pandemic, down by 10% from 2011. Then there was a very large reduction during and after the pandemic, so that average journey lengths on Advance tickets are now a third of those in 2011. While this may be due to split ticketing, we have also seen Advance tickets now being sold for some very short journeys, for example, Stockport to Manchester.

Anytime peak and off-peak tickets have showed broadly the same pattern, with average journey lengths declining by 20% from 2011 until the pandemic. Since the pandemic, peak fare journey lengths have remained constant while off-peak journey lengths have continued to decline. Again, it is difficult to determine whether it is the impact of split ticketing or other factors that have driven changes in journey length.

Figure 6: Index of average journey length by ticket type, four quarter moving average Jan-Mar 2011 to Jan-Mar 2024.

Source: Office of Rail & Road https://dataportal.orr.gov.uk/statistics/usage/passenger-rail-usage/

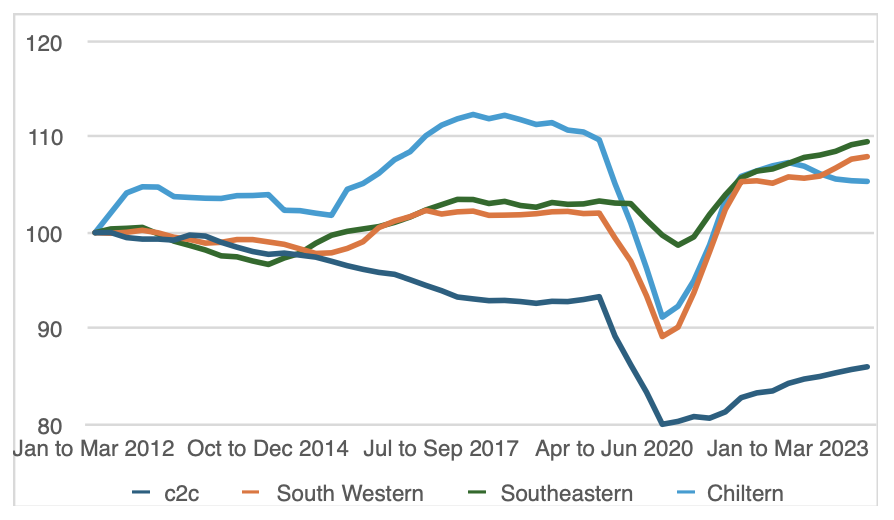

The final set of analysis considers average journey length by train operator. This is complicated by changes in TOC boundaries and service patterns. Figure 7 considers some of the London-focussed TOCs. Shorter journeys are less likely to be subject to split ticketing and hence changes in average journey lengths are likely to be driven by different factors. Chiltern saw average journey lengths increase as they grew their longer distance services between London and the West Midlands. South Western and South Eastern saw relatively little change in average journey length until the pandemic, after which they increased, contrary to the picture seen in figure 5. C2C on the other hand saw a steady decline in journey length, possibly a combined impact of more local trips due to timetable changes and some people travelling to Canary Wharf rather than the City of London.

Figure 7: Index of average journey length by TOC, four quarter moving average Jan-Mar 2012 to Jan-Mar 2024.

Source: Office of Rail & Road https://dataportal.orr.gov.uk/statistics/usage/passenger-rail-usage/

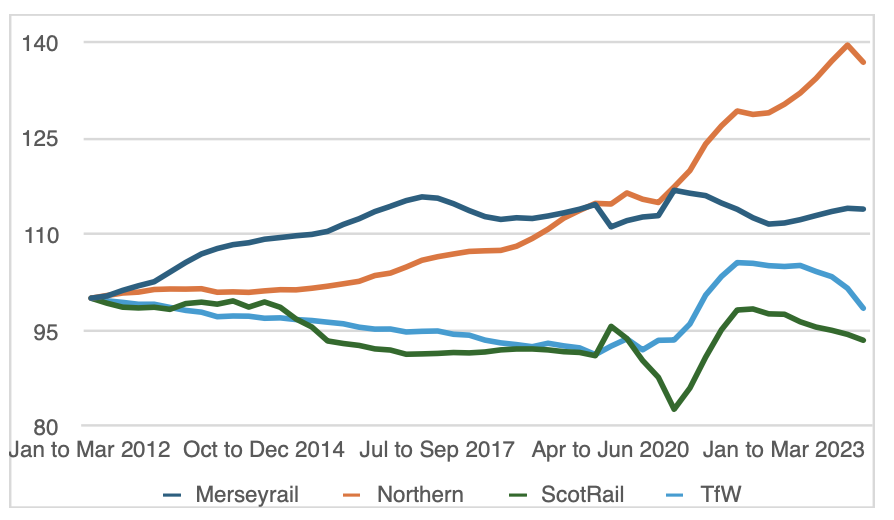

Figure 8 considers some of the regional TOCs. Northern is the standout here with a considerable increase in average journey length of around 15% up to the pandemic, and after that a large increase. Average journey lengths are now 40% higher than in 2012. The decline in short commuter trips into Leeds and Manchester is probably the reason for the post pandemic situation. Merseyrail average journey lengths steadily increased until 2017, after which they remained constant, which is not surprising given the nature of the network. However, there are still issues with how tickets sold within the erstwhile Passenger Transport Executive areas are recorded, which may also impact the analysis. Scotrail and Transport for Wales had a steady decline in average journey lengths until the pandemic. They then saw a major increase afterwards, but have now returned to their steady decline. Changing travel patterns rather than split ticketing is likely the main factor behind changes in journey length for these TOCs.

Figure 8: Index of average journey length by TOC, four quarter moving average Jan-Mar 2012 to Jan-Mar 2024.

Source: Office of Rail & Road https://dataportal.orr.gov.uk/statistics/usage/passenger-rail-usage/

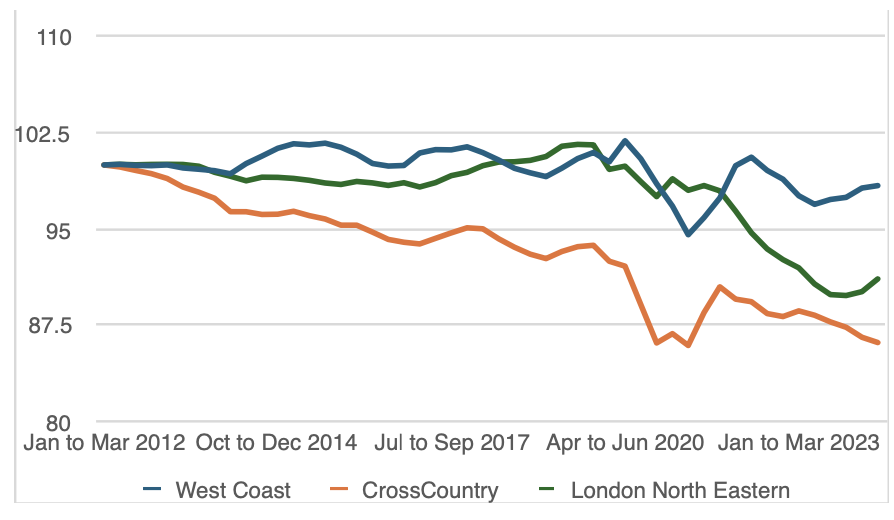

Finally figure 9 examines TOCs that typically see longer journeys and hence are more likely to experience split ticketing. Due to its fare structure, Cross Country reportedly has higher than average rates of split ticketing. As can be seen, average journey lengths on Cross Country have fallen, and particularly steeply so since the pandemic. West Coast and London North Eastern saw little change in average journey lengths up until the pandemic. Since then, London North Eastern has seen a marked decline in journey lengths while West Coast has seen little change. Lumo’s impact on very long-distance trips on London North Eastern may be a factor here, as have service reductions by other operators serving the North East leading to an increase in short trips on its services. Split ticketing is also thought to be increasing on this route.

Figure 9: Index of average journey length by TOC, four quarter moving average Jan-Mar 2012 to Jan-Mar 2024.

Source: Office of Rail & Road https://dataportal.orr.gov.uk/statistics/usage/passenger-rail-usage/

In summary, eight TOCs have seen a reduction in average journey length since 2012. Some operators, like C2C and Thameslink, are unlikely to be significantly impacted by split ticketing. Cross Country and London Northeastern, which have seen the largest decrease in average journey length, are likely impacted by split ticketing. However, the impact here in terms of journey numbers is likely to be immaterial.

Overall, if average journey lengths for long-distance trips were the same in 2023/24 as before the launch of split ticketing by RailEasy, then there would be 130 million instead of 135 million such journeys. While for the whole network there would be 30 million fewer recorded journeys, down from 1,610 million to 1,580 million. In effect split ticketing might be over inflating the number of rail journeys by 2% across the whole network.

The ORR is working with the Rail Development Group, the industry co-ordinating body, to improve its published estimates by incorporating an adjustment for split ticketing to more accurately reflect the actual number of journeys made.

As the railways come back under public ownership more data is being put into the public domain. This includes individual train load data for some TOCs which is being published on the Rail Data Marketplace (https://raildata.org.uk/). While the data is presently not complete or highly accurate it offers the potential for more timely and comprehensive analysis of how rail is performing in terms of patronage.

References

The data reviewed in this article and charts can be found at:

Office of Rail & Road https://dataportal.orr.gov.uk/statistics/usage/passenger-rail-usage/

John Siraut is director of economics at Jacobs.

This article was first published in LTT magazine, LTT903, 13 November 2024.

You are currently viewing this page as TAPAS Taster user.

To read and make comments on this article you need to register for free as TAPAS Select user and log in.

Log in