TAPAS.network | 2 April 2025 | Commentary | Stephen Glaister

Some warning signals for the government’s plan for Rail Reform

Professor was chair of the Office of Rail and Road from 2016 until 2018 and has studied and commentated on rail industry issues and different ownership and delivery models. Here he looks at the Government’s rail reform plans, and where outcome expectations may be optimistic with particular potential problems in the framework for ultimate control and decision-making

BRITAIN’S HEALTH SERVICES and railways are the country’s two largest public sector enterprises, with 1.3 million and 220,000 employees respectively. Reform is on the way for both. One of the explicit aims of the utility privatisations of the 1980’s and 1990’s, and of the previous set of NHS reforms, was to reduce the ability of ministers to micro-mange because the experience had not been good. Now the tide is running strongly in the opposite direction, for the way both the NHS and the railways are to be run. There may be different considerations in each case, but for those of us in the world of transport it is surely worth us asking if ministers should really want to run the railways - and are they likely to be any good at it if they do?

In March the government announced reforms to the governance of the National Health Service involving abolition of arms-length bodies and giving the Secretary of State close responsibility of both high-level policy and delivery. Meanwhile, the government had published a Consultation (ref 1) in February on its proposals to legislate to reform the railways in Great Britain. The government intends to create a single body under the direct supervision of the Secretary of State: “The Secretary of State will have the power to issue directions and guidance … enabling the government to drive performance and improvement where appropriate through proportionate and strategic interventions.” But it is vague about the extent to which those responsible for the delivery of rail services would have operational independence. If the spirit of the latest announcements on the NHS is taken as an indication for the railways, the proposals may bring all Great Britain’s railway activity (except rail freight and Transport for London) into a single sub-department of the Department for Transport and there could be less independence than there has ever been, including the Nationalised Industry, British Railways 1947-1993.

Origins of the reform

In May 2018 the railway tried to make a major change to the timetable so as to improve services for the benefit of passengers, including the opening of new Thameslink infrastructure and a significant change to cross-London service patterns. Chaos ensued in two parts of England with many delays and cancellations, and knock-on effects were felt across the national network. Passengers suffered significant financial and emotional cost and trust in the railway was undermined.

Consultation on the rail reform legislation began under the last government in 2022, was the subject of a Labour Party policy document last year, and is now hopefully being finalised

Secretary of State Chris Grayling asked the independent Office of Rail and Road to conduct an inquiry to establish what had gone wrong, which I chaired (ref 2). He then commissioned Keith Williams to conduct a “sweeping review to transform Britain’s railways (ref 3)”. When he reported, the then Secretary of State Grant Shapps appended his name to the proposals tabled by the Government in a white paper in 2021 as the Williams-Shapps plan, and though suitable legislation was promised to enact the provisions, none had been tabled by the time the last Conservative Government left office in 2024. The current consultation (closing on 15 April 2025) on legislation about to be considered by the new Parliament, and made a key element in its Election manifesto, is the new Labour government’s response.

The main problems on the railway, which were apparent six years ago and before the Williams Review, included: taking a grip on the administration of a working, reliable timetable; determining allocation of scarce track capacity between local passenger services, long distance passenger services and freight; problematic industrial relations; poor procurement and management of contracts for passenger services; appropriate passenger representation; keeping effective control of cost efficiency; and, above all, finding enough public money to meet everybody’s aspirations for a cheap, high quality service. Williams added: giving strategic direction; long term thinking and innovation; clarifying accountabilities and bringing decision-making closer to users-including devolution away from the centre.

The proposed, monolithic institution (Great British Railways, GBR) will have broad responsibilities: to simplify passenger fares and set the levels; to plan and operate the timetable; to determine which passenger services run—and therefore determine the beneficiaries of a great deal of public money; to determine which train operators get access to the infrastructure—passengers, freight, competitive open access passenger services, local authority-sponsored and devolved administration services; to determine the terms of access including charges; to plan and seek funding for new investments, and manage them to “to ensure benefits from investment are delivered”; and to take liabilities for borrowing from both public and private sectors.

Before the proposals can be assessed there will surely have to be more detail about the governance structures: how will GBR and the Secretary of State be held to account to government, parliament and the tax-paying public? One of the issues is the extent to which the new structure is designed to keep ministers away from the day-to-day running of the railway. Another is the effectiveness of the disciplines and incentives on GBR to keep it functioning economically, efficiently and in the public interest, rather than in the sprawling management’s interest in “a quiet life” and in the vested interests of the employees—problems that were not solved the last time any of our big utilities were state-owned Nationalised Industries.

Managing changes to the timetable

The railway is an inter-related system of many activities. The timetable has to be painstakingly designed so as to permit trains to run without interfering with one another because track and station capacities are limited, and to allow interchange as effectively as possible between services so the network works as a whole. Unless a margin of redundancy is built in the inevitable random perturbations will cause the whole service to become unreliable. It takes time and effort to design-in any change and for that reason there is a strict protocol concerning the advance dates by which requests for alterations must be made by the passenger and freight operators or by the Department for Transport (DfT). There is currently a “System Operator” within Network Rail that works out what can be accommodated and, in cases of conflict, decides which trains can enter the timetable and which cannot. Users that are refused access can appeal to the independent Office of Rail and Road (ORR). ORR determines the charges for access.

By May 2018 discipline had lapsed and protocols were not being observed: late requests from train operators and from ministers were considered. On the day of the change that caused all the trouble the timetable was not robust. Operators had not had enough time to assure themselves that they had the working infrastructure they had planned for, and that they would have sufficient rolling stock and—particularly—enough appropriately trained drivers. The System Operator, working with good intentions under enormous pressure knew there were problems, but had not felt empowered to enforce the agreed procedures and say ‘No.’ Nobody took charge (ref 4).

The failings were quickly recognised. Network Rail increased the resourcing of its System Operator function and re-established observance of the protocols. The problem was largely resolved.

Industrial Relations

A second problem became critical as train operators struggled to restore a half-decent service. The long-standing, varied and complicated working agreements with the staff limited operators’ ability to adjust quickly and use their staff in different ways at short notice. Also, the agreed procedures for recruiting, training and qualifying more drivers on the specific routes took a long time to complete.

Ever since, unusual labour agreements such as the practice of relying on voluntary rest-day working, and industrial action because of disputes have continued to have a damaging effect on the reliability of services to passengers.

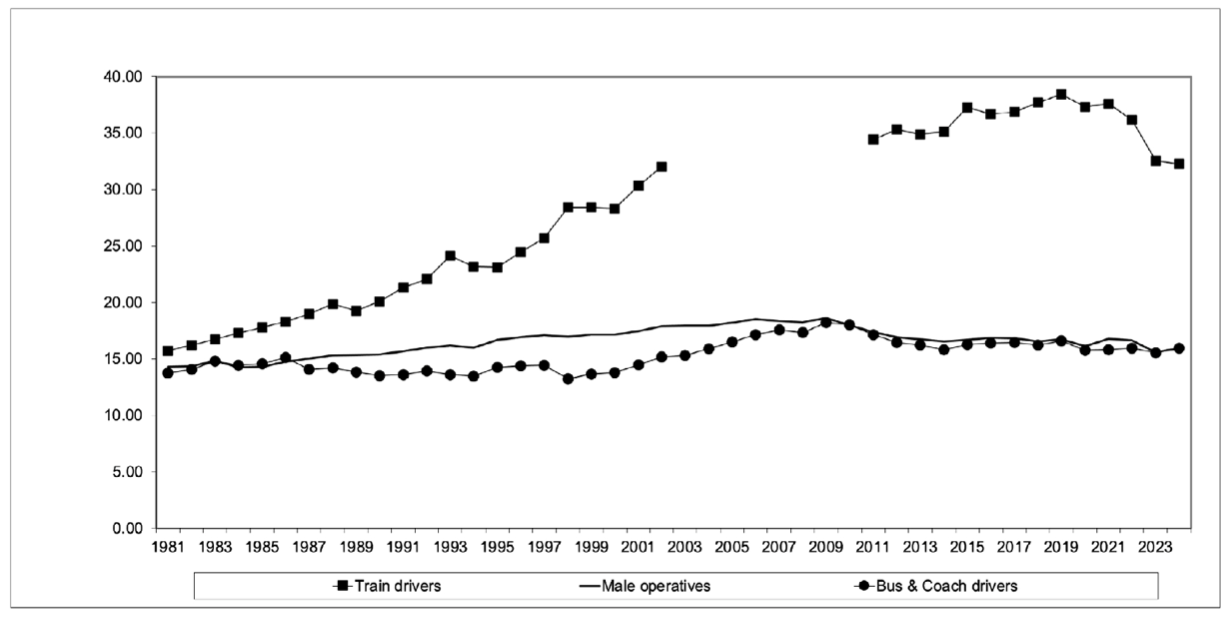

One of the objectives of the introduction of competitive tendering of bus services in London from 1984, of the deregulation of the bus industry outside London in 1985 and of the 1993 fragmentation and privatisation of the railways was to introduce competition in the respective labour markets. This, it was hoped, would bring earnings in line with those in similar occupations. Figure 1 shows average hourly earnings since 1981 for bus drivers, train drivers and all similar occupations (male, Standard Occupational Classification 8) adjusted for inflation by the Retail Prices Index.

Figure 1 suggests that before the 1985 bus deregulation, bus drivers’ hourly earnings were close to the average. After deregulation they were pushed below the average until about 2010, after which they ran close to the average again. But in the case of railways, in 1981 hourly train drivers’ earnings were above the average and the gap increased steadily until 2020 when they were more than twice the average. There is little evidence of any effect of the 1993 reform. It is apparent that, unlike the bus industry, the agreements negotiated by the rail unions and managements succeeded in keeping train drivers’ average hourly earnings well above comparable occupations.

Figure 1. Average hourly earnings (2024 prices). £ per hour.

Source: Office for National Statistics, Earnings and hours worked, occupation by four-digit SOC. Train drivers’ earnings were not reported separately between 2003 and 2010. These figures include London Transport train drivers and tram drivers.

There is only passing mention of this topic in the rail reform Consultation. Whether or not there are to be structural reforms of the railway, the problems with the terms and conditions of employment and the need for better long term planning of qualified employee resources have to be addressed, both in the interest of delivering a full and reliable set of services for passengers and in order to contain costs in the industry. Presumably the government rather optimistically hopes that it can rely on “the public sector remit will apply” without suffering crippling industrial relations disputes.

Passenger service procurement

Under the present system most passenger services have been specified by the DfT and until recently the Department procured them from private companies under commercial contract. There is a general agreement that this process has been problematic. Partly this was because of DfT falling to the temptation to accept unrealistically optimistic bids from train operating companies and then having to bail out failed contractors; and partly because of DfT failure to manage contracts firmly to hold surviving operators to their promises. This defeated the competitive incentives on operators to behave economically and efficiently whilst delivering services to specification. If not exactly ‘too big to fail’, the idea of regularly changing failing operators was not at all appealing to the DfT.

Under the new proposals the operating function will be taken over by GBR and the services will be provided “in house”. It is an open question as to whether this will be more successful. It will almost certainly be less transparent to parliament and the public. The experience with the highly successful competitive tendering of contracts for individual London bus services illustrated how the instigation of transparent, explicit agreements properly enforced can, in itself, improve service quality. Actual service delivery had to be measured and recorded properly and people could be held to account for service failures, rather than letting them go unremarked (ref 5).

Money

Passengers naturally wish to have more and better quality services at lower fares, and freight shippers would like to pay lower charges and gain better access to the system—and that would help with the aspiration to shift freight from road to rail. However, these things increase the call on the taxpayer and the Treasury is pressing hard to reduce public spending.

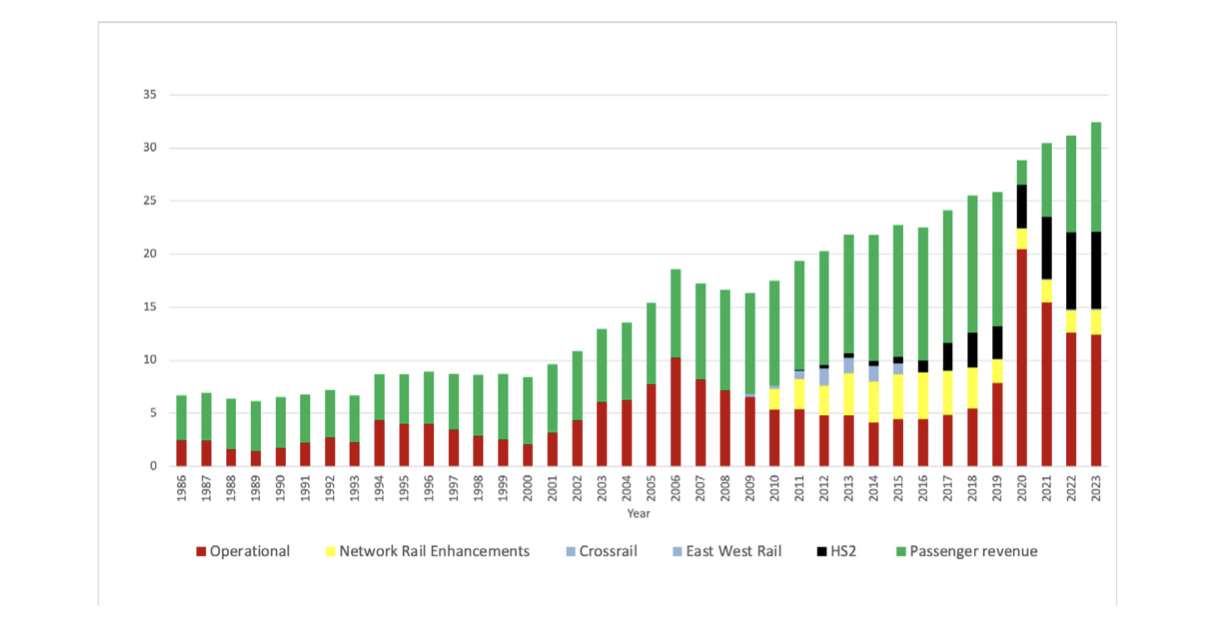

As shown in Figure 2 government support stood at £22.3bn in 2023-24. This included £12.5bn of operational funding to train operators and Network Rail, £2.3bn to Network Rail for enhancements and £7.3bn to HS2. That was a significant call on the Exchequer—over £400m per week, or £700 per household in that year.

Figure 2 shows that support rose in the lead-up to the 1993 rail reform and then fell up to 2000. Then after the effective nationalisation of Railtrack to form Network Rail support rose steadily to £10bn in 2006-07. For the decade from 2009 support, including grant for Network Rail enhancements (but excluding Crossrail and HS2) was between £7bn and £10bn pa.

Figure 2. Government support to rail industry passenger revenues (constant 2023-24 prices). £bn

Sources: Office of Rail and Road, table 7270 and table 1210. Additionally, between 2015 and 2023 revenue from rail freight companies was about of £1bn pa.

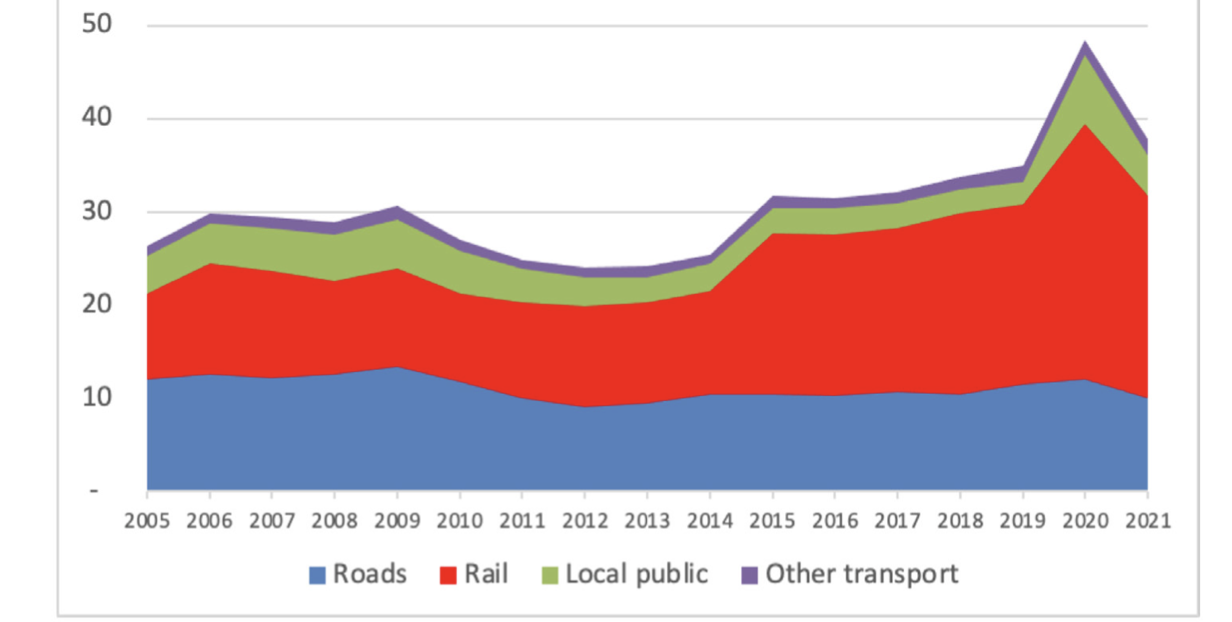

Figure 3 puts government spending on the railways in context of spending on all surface modes. In 2019/20 (before the Covid pandemic) road taxation yielded about £35 billion so it was of a similar magnitude to the total of the total of government spending on roads, railways and other transport. In those years national rail carried about 10 percent of all mechanised passenger miles compared to roads’ 90 percent, and rail carried a similar proportion of freight-tonne km. So, broadly speaking, roads were providing for nine times the mechanised movement as rail and roads taxation was sufficient to cover the roads’ own direct expenditures as well as the subsidy to rail. It is particularly striking that support for local transport (including buses) has become such a small proportion of the total.

Figure 3. Public Expenditure on Transport in GB, 2005/6–2021/2 (2020-21 prices). £bn

Source: David Bayliss, “Motoring Towards Net Zero—Old Problems and New Challenges”, Journal of Transport Economics and Policy, October 2023.

In the current financial climate it seems more likely that the level of financial support for rail will fall than be increased in the near future.

The government has said that it wants to simplify the fares structure. That sounds attractive, but there are downsides. Fares are complicated because in recent years train operators have been increasing the financial yield from their sales by using the same dynamic pricing techniques that airlines and hotels use. This is price discrimination and if there were sufficient subsidy available to allow fares to be matched to costs then it would be in the public interest to eliminate it. However, as things stand with strictly limited public funds available, price discrimination is a useful way of meeting constrained budgets whilst minimising loss of unremunerative services. ‘Simplification’ will potentially reduce the revenues—unless there was a compensating increase in the overall, average rate of charge per passenger mile. Another, distinct reason for variation is matching charges to varying costs: for instance offering cheap deals at times and places when there would be a lot of unused seats. That allows passengers to benefit rather than allowing them to go to waste. Simplification could reduce such scope to match fares to economic circumstances.

If the reform were successful in reducing unit costs in the industry then funds would become available for alternative uses. However, after a number of independent efficiency reviews over recent years—including the scrutiny by the independent Office of Rail and Road as part of the periodic review process—it would be unwise to rely on yet more efficiency improvements. Some commentators have asserted that nationalisation will produce cost efficiencies because the payment of “profit” to the private train operating company owners would be avoided. That neglects the fact that this “profit” is, at least in part, a return on their capital invested. In the public sector, capital does not come free either—it appears as an addition to the national debt, which has to be serviced by the taxpayer. The public sector cost of debt (the rate of interest) may be lower than the private sector rate: on the other hand others have asserted that any benefit from that is overwhelmed by the loss of transparency, commercial management and incentives which will make it harder to deliver cost efficient management.

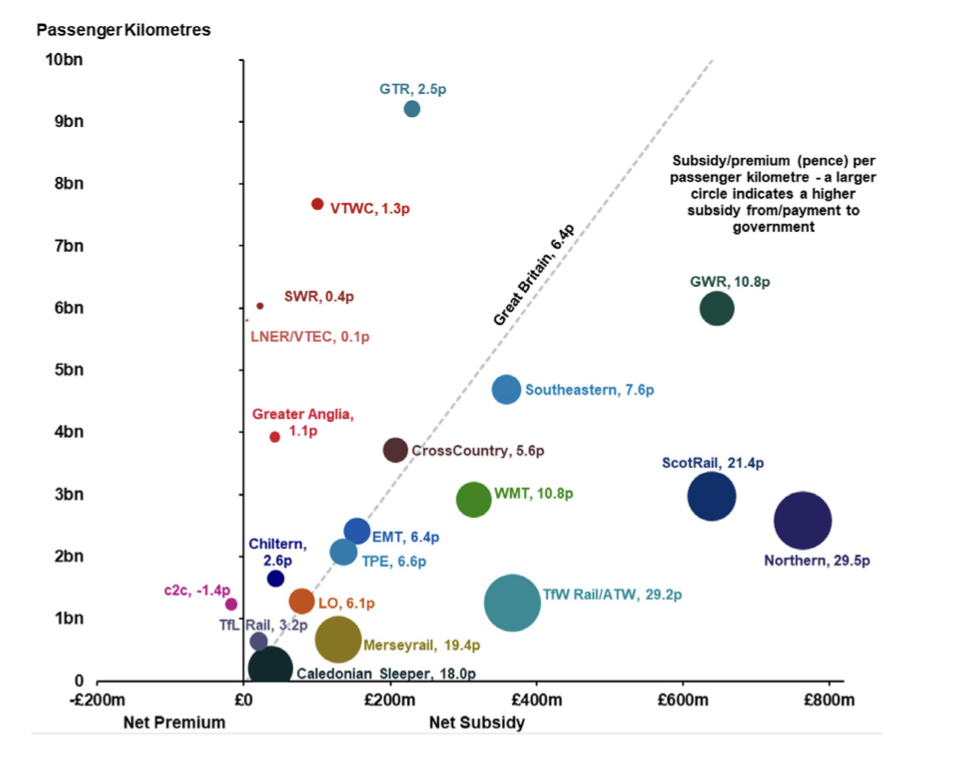

An alternative way of freeing up funds would be to decide that not all of the present, loss-making activities can be continued, and the network adjusted accordingly. The rail taxpayer subsidies are unevenly distributed amongst the users of the different rail franchises, as shown in Figure 4, issued by the Office of Rail and Road. These data relate to 2018-19, so before Covid and there will have been changes since. However, they remain illustrative of the wide range of beneficiaries from government support for the railways. The national average was 6.4 pence per passenger km. as represented by the 45-degree, dotted line. Franchises to the right of that line are in receipt of higher than average subsidies per passenger km. The size of each coloured “blob” is proportional to the subsidy per passenger km for the respective rail passenger franchise and the position on the horizontal axis represents the absolute level of subsidy for the franchise.

Figure 4. Net government support per passenger kilometre by train operating company, Great Britain, 2018-19

Source: “Rail Finance 2018-19”, Office of Rail and Road, 14 November 2019, https://dataportal.orr.gov.uk/media/1547/rail-finance-statistical-release-2018-19.pdf

Three franchises had high absolute subsidies and high subsidies per passenger km (and therefore few passenger km in relation to the absolute subsidy): Northern (29.5 p/km), ScotRail (21.4p/km) and Wales (29.2 p/km). So, as one might expect, the highest rates of subsidy went to passengers in the generally sparse, rural regions. Rather as the situation facing Beeching when he was asked to recommend ways to improve the railways’ finances in the early 1960s, a large portion of the financial support was being consumed by relatively lightly-loaded franchises.

In the circumstances the extreme levels of subsidy in some cases may not have sufficient justification and the same money might be used more beneficially. Unsurprisingly, the Consultation does not discuss this possibility.

Reform of system operation

The Consultation paper correctly recognises the importance of the System Operator: “Dealing with these complex problems needs an empowered, cohesive body with oversight over the entire system …”

However, in the new regime there will still be just as many “interfaces” between different activities in the railway—such as train operations, rolling stock provision, track maintenance, competition for track and station facilities, employees and labour agreements. It is just that they will be managed internally, and less transparently, within GBR. The bureaucratic costs of fault attribution will be avoided, but it will be important to preserve the benefits that fault attribution was designed to create: record keeping, understanding of causes of service failure, accountability and incentives to avoid causing failures.

The Consultation Document asserts: “In its role as the ‘directing mind’, Great British Railways (GBR) will bring track and train back together and plan services on a whole-system basis, to better deliver for passengers, taxpayers, and freight customers, and to unlock growth. This will include working closely with devolved leaders and local partners, drawing on their experiences and expertise. … They need the ability to create unified transport networks that serve their cities and regions much like Transport for London....” We should note, incidentally, that this fails to acknowledge that whilst Transport for London does own and control the Underground and the Overground made up of some of the former national network lines, it still does not have any control over much of the rest of the railway that serves the wider conurbation—much to the despair of successive mayors.

Although the single ‘directing mind’ is so frequently hailed as needed by ministers of all persuasions the same conflicts will remain between local passenger services, longer distance passenger services and rail freight because not all demands can be accommodated. It is not clear how the new proposals will find capacity that the existing System Operation has not been able to find.

The government is claiming that the new structure gives it a “method to ensure benefits from investment are delivered”. The Consultation does not exactly articulate how the new structure under the Secretary of State would “ensure” this more effectively than under the current regime.

The Consultation is hopeful that timetable planning can become more flexible and responsive: “…an excess of legislative and contractual process has led to a system which is inflexible and discourages improvement and innovation. …” However, it was the attempt to become more flexible by relaxing the strict protocols for managing changes to the timetable that precipitated the May 2018 disruption. The lesson of May 2018 was that in a system as intensively used as GBR, changes have to made carefully and strictly in accordance with an agreed process. In fact, left to its own devices the timetabling authority would have an incentive, in an abundance of caution to slow things down and build over-generous recovery time into the timetable, giving priority to reliability rather than to journey speed or system capacity.

Access

GBR is to take over ORR’s decisions on access terms including charges and incentive regimes, and GBR is to be subject to directions from the Secretary of State. Access to GBR’s network is meanwhile required for a significant portion of other railway activity: all freight, passenger services in Scotland, Wales, Liverpool, parts of London as well as any newly-devolved authorities. There are additional open access services such as those by independent passenger train operators such as Hull Trains and Lumo Trains.

In the current system, rights of access and the resolution of conflicting claims on it, are considered by the independent ORR in accordance with its statutory powers and duties. The experience has been that every time the ORR has received an application for new open access passenger services the Department for Transport has argued against in the strongest terms, mainly because of fear of abstraction of revenue from DfT-sponsored existing services. DfT has given little weight to the argument that new services can generate new benefits and extra revenues. It typically also argues that there is not enough capacity so reliability of existing services would be compromised. In other words, it has no hesitation exploiting a monopoly position (by seeking to deny competitive services) to protect its own revenues, without regard to the consumer benefits of extra, cheaper services. In some cases the ORR has found that there is, in fact sufficient capacity and has allowed access in the public interest.

Although the Consultation says that “the new legal framework will be designed to unlock the benefits of the proposed new access regime in a way that ensures fairness and transparency for passenger and freight operators”, on past form it seems unlikely that new open accesses passenger services will be tolerated by DfT. There is an indication that better, and more long term access will be allowed to freight services, but that begs the question of which passenger services will be denied access to create the necessary space, and according to what criteria.

GBR will take initiative in proposing train service changes and GBR, rather than the independent ORR, will set access charges for non-GBR services that are “fair and non-discriminatory” and cost reflective. Judgements about what is “fair and non-discriminatory” will no longer be taken by an independent body (though there will be appeal to the ORR). GBR will able to give discounts against cost-based charges to deliver government’s strategic goals, and the Secretary of State will have the power to guide and direct. These are important changes.

Governance

The proposal is to create a single, large organisation covering the nation. Formal, legal governance is crucial. The railways were once a collection of shareholder businesses, then a Nationalised Industry, then a collection of privatised companies with the essential network-owner (Railtrack Plc) subject to independent regulation, then the network owner became a Company Limited by Guarantee which, in turn came back under direct government control in 2014. Each of these legal structures had its own implications for the powers and duties of the company boards. Each structure mattered in terms of accounting standards, legal competency to borrow, requirements for transparency, incentives for efficiency and accountability to parliament and other funders.

Crucially, the Consultation is not explicit about what is proposed, though some kind of “arms-length” body within the Department for Transport is implicit: “GBR will be held to account first and foremost by the Secretary of State though its Chair and Board.” It appears that the “arm” may be substantially shorter than it is under the current arrangement.

The Consultation makes it clear that the government is going to take firm and direct control on how scarce capacity will be used : “the Secretary of State can issue specific Directions and Guidance on access to and use of the railway when relevant, for example to emphasise the priorities of certain regions or cities, or markets such as freight”.

Similarly, the Secretary of State will ultimately be responsible for charges and what open access will be allowed. And in determining passenger fares and the pattern of passenger services offered GBR will implicitly determine the beneficiaries of large amounts of public money as illustrated by Figure 4 above.

There is no doubt that GBR, under the direction of the Secretary of State will be required to make important decisions in the public interest. The consultation document makes this clear :

“A new and simpler framework will enable GBR to take decisions on the best use of its network, putting the interests of passengers and freight customers first while providing certainty that the benefits of investments will be realised … under the new access framework. GBR’s access and use functions will be governed by its duties to deliver whole system benefits, government priorities, and the goals of devolved governments and Mayoral Strategic Authorities. …GBR will have a clear remit set in statute empowering it to focus on delivering national benefits. … GBR will take access and charging decisions in the public interest … New statutory duties will ensure that GBR’s access decisions… will ensure fair treatment for all operators wishing to access the GBR-managed network. GBR will… focus on delivering national benefits …. To the extent that decisions are not entirely in the gift of ministers, the governance of GBR will need to be clear how GBR will be held to these important ideals.”

When the Consultation says that “GBR will take account of the long-term strategy set by the Secretary of State … These obligations will enable GBR to reflect funder priorities for the use of the railway on relevant routes” it would be helpful to remember the unsuccessful experiences (ref 6) of the Strategic Rail Authority (SRA) that existed between 2000 and 2006 under the last Labour Government to provide strategic direction for the industry under the motto ‘Britain’s railway, properly delivered’. A major problem was that the SRA chair and board felt that they had a duty to promote a bigger and better railway, whilst HM Treasury felt that it was being landed with unauthorised long term public expenditure liabilities that it could not control: the SRA did not survive.

It is welcome that the government commits to the continuation of the five-year planning cycle, where it says what it wants in the High Level Output Specification and how much money it is committing to achieve that in the Statement of Funds Available, and the independent ORR adjudicates whether those are consistent. Currently, once all this has been reconciled and signed off by the ORR there is a degree of certainty for the industry for the five-year control period—this is helpful to the industry and quite unusual in the UK public sector. The Consultation gives a less welcome hint that this certainty may be weakened when it says “The proposed legislation would preserve flexibility and allow for the scope of activity funded by the settlement to change over time where this may allow greater benefits to be delivered.” The current experience of the strategic road network offers a worrying precedent: this could quickly revert to the year-by-year public sector budgeting which is so damaging to effective management of infrastructure industries with very long-lived assets.

One of the indisputable benefits of past rail reforms since the Nationalised Industry days has been the collection of more generally visible, granular information and, in particular, detailed financial accounts compiled to modern, widely accepted standards. It is important that these standards are retained and independently enforced, and that we do not revert to the fog of the old public sector-style accounting.

As now, there will be a licence issued by the Secretary of State (to GBR rather than to Network Rail) and enforced by the ORR—and, also as now, there will be the awkward issue of how meaningful it is for ORR to enforce, presumably through fines, against a publicly owned and funded body.

Private investment

A major motivation for the 1993 rail reform and the 1996 privatisation of the main infrastructure owner, Railtrack, was to take capital investment off the “public balance sheet” and to transfer the responsibility for it to the privately-owned rolling stock owners, train operating companies and Railtrack. One of the statutory duties of the independent ORR (like all the utility regulators) was—and remains—to ensure that investments by regulated entities that are economic and efficient will be duly remunerated (although the rolling stock companies, suppliers and freight operating companies fall outside its remit). In other words, there was a clearly defined and well-understood structure of company governance and an independent regulator to protect investors from the whims of political influence in the railways.

But the shareholder company, Railtrack Plc went into administration in 2002 and was replaced by Network Rail, a company limited by guarantee and then, in effect, nationalised in 2014. The wish to attract private capital to the infrastructure has nonetheless remained, as illustrated by Network Rail’s 2018 “Open for Business” campaign (ref 7). However, the aspirations to attract private capital have not been fulfilled on the scale that had been hoped.

Unless the government clarifies the governance of GBR and the relevant powers and duties of the ORR, it seems likely that there will be less private investment than in the past. The rolling stock companies and freight operating companies may well continue as investment opportunities, but it is unclear what investable opportunities there may be in passenger train operation or fixed infrastructure.

The passenger voice

The government headlined its consultation with “New rail watchdog to give passengers a voice and hold railway to account”, but what is proposed is not very different from the existing arrangement. The new body is to be advisory and could be seen as a better-resourced development of the existing customer representation body Transport Focus. Meanwhile the previous Secretary of State who was architect of the new rail industry plan for Labour, as it prepared for Government, frequently expressed her wish to play the role of ‘Passenger in Chief’. There will be a Rail Ombudsman as there is now, under the new structure.

Conclusion

The railways have been reformed regularly: 1921, 1947, 1963, 1993, 2001, 2014. Each time the new structure worked well enough for a period before the government of the day intervened, discovered it could not achieve its political or financial objectives and then tried a new system.

These experiences have illustrated the importance of being realistic about the amount of taxpayer funding likely to be available for a number of years into the future, about cost efficiencies, and given these, the fares and services that can be delivered.

Whether or not there is further reform, one feature of the present system is worth keeping: the certainty of the five year funding cycle. Longer might have been better, but what exists is unusual in the public sector. There is a hint in the Consultation that it might become easier for ministers to change budgets at short notice. Also, to protect the cost base of the industry and improve reliability of services, the terms under which labour is employed need to be rationalised.

Before the present proposals can be made successfully operational there will have to be clarity about governance, in particular the role of ministers in running the railway. There needs to be clarity about the promotional and development role of the System Operator and that it will be allowed to do its job. The government needs to explain how its proposals will deliver the benefits they expect such as better investment planning and that empowered local business units will better serve local communities. It also needs to explain how sufficient track capacity will be found for the rail freight it wishes to promote, including catering for economic growth. Similarly it will have to specify clear criteria by which decisions can be made to resolve conflicts between the demands of devolved authorities for passenger capacity and centrally-determined services. To state an aspiration does not make it happen.

Above all, incentives matter. It is vital to have a clear system of governance and that people are held accountable. Generally it has not worked well when ministers have become frustrated and intervened with management at a level below the strategic. Many structures can be made to work, but only if they are left to function as designed and not compromised.

Around the world the tensions over rail have often reflected the difficult mix of elected politicians, civil servants in the ‘ministry of railways’, and the different enterprises responsible for the track, and the running of the trains. Having a single entity ‘in charge of everything’ has its theoretical appeal, though perhaps unsurprisingly, has rarely removed the obvious stress points in this exceptionally complicated industry.

References and Links

-

“A railway fit for Britain’s future”, 19 February 2025 https://assets.publishing.service.gov.uk/media/67b30e36b56d8b0856c2fd49/a-railway-fit-for-britains-future.pdf

-

Interim and final reports. https://www.orr.gov.uk/monitoring-regulation/rail/investigations/may-2018-network-disruption

-

https://www.gov.uk/government/news/government-announces-root-and-branch-review-of-rail

-

Kennedy, David. 1995. “London bus tendering: a welfare balance,” Transport Policy. Volume 2, Issue 4, October 1995, Pages 243-249

-

Terry Gourvish, “Britain’s Railways 1997-2005”, Oxford University Press, 2008

Stephen Glaister is Emeritus Professor of Transport and Infrastructure in the Centre for Transport Studies at Imperial College London and visiting professor at the London School of Economics.

He has specialised in the economics of transport and its regulation. From 2015 to 2018 he was Chair of the independent Office of Rail and Road, and was a Board Member of Transport for London.

He was a member of the Government’s first Advisory Committee on Trunk Road Assessment and he has been an advisor to the Parliamentary Select Committee on Transport and to the DfT and other bodies. He has published widely on transport and utility regulation. He was also Director of the RAC Foundation.

This article was first published in LTT magazine, LTT912, 2 April 2025.

You are currently viewing this page as TAPAS Taster user.

To read and make comments on this article you need to register for free as TAPAS Select user and log in.

Log in